TL;DR

In short

- Let’s start with some basic facts.

- For more localised analysis, we can use ad portals like Rightmoveand Zoopla.

- In the previous paragraph I mentioned that real estate prices are gently lower than in previous months.

- Property prices expressed in pounds are now really high.

- In addition to the official UK House Price Index, there are several other equally useful indices.

Today’s article is rather an overview - instead of explaining more, we’ll cover the topic of prices in the UK property market. Of course, this information will be of most use to those who are planning to buy or sell a house in the UK, but I think it will also be interesting to read for those who have no desire to move anywhere :)

What will property prices be like in the UK? What’s happening in the market?

How do we know what current property prices are?

Let’s start with some basic facts. First and foremost, property prices are dynamic - buyers adjust to a volatile market on an ongoing basis, while negotiations between the parties to the transaction are possible at the purchase stage. Unlike 2023, inflation is no longer as high and high interest rates have reduced interest in the property market. The best evidence of this is the UK House Price Index, calculated by the Land Registry.

According to the latest, or November, UK House Price Index report, the average price of a house in the UK was £289,707, up more than 4% on January 2024, but down 0.9% on the record-breaking August when the average price was as high as £292,501.

With the impending changes to Stamp Duty Land Tax, you may be seeing some price rises. The Rightmoveportal, in its January report, showed that the average house price rose to £366,189 in January. This is a jump of 1.7% compared to December, when it was at £360,197. It is worth noting that the November figures we reported earlier are for the average price of all property types. Unfortunately, official sources such as the Office for National Statistics (ONS) do not provide updated reports.

Where else can we get data from?

For more localised analysis, we can use ad portals like Rightmoveand Zoopla. Not only will you find tools and reports on the locations you are interested in on these sites, it is worth simply analysing the database of current listings - always a sure indicator of the market situation. While we are on the subject of offers, it is worth recalling our article explaining how to increase the value of a property when selling. At the bottom of the post, you will find more information about online valuation tools.

You can also ask your real estate agent and mortgage broker about current property prices, although it’s fair to say that no one will give you a very precise answer. Such statistics are usually public, and an analysis of our recent transactions may not be the most accurate, after all, we operate on a small scale for the entire market. Of course, any broker will tell you that real estate prices have been fluctuating for the last year, but giving specific figures would already be very difficult.

Over the past six months, real estate prices have gently increased, but we still haven’t managed to return to record levels. While this is of great importance to buyers, without in-depth analysis it will be difficult to realize that something has changed. Announcements are constantly changing, and the differences in prices are not large enough for the market to experience rapid changes. If the average dropped by £50,000, you would certainly hear about it in the media.

Will UK property prices fall?

In the previous paragraph I mentioned that real estate prices are gently lower than in previous months. Does this mean that there will be a crash in a while, and houses can be bought for a fraction of the price? No, although further gentle declines are possible. According to the latest statistics from December 2024, inflation in the UK is already at a quite acceptable level, although it has increased by 0.4 percentage points compared to May 2024. Consequently, sellers’ expectations are also changing. I would, however, be very cautious about saying that property prices will decline markedly. After all, it’s important to remember that even if inflation were to fall to 0% now, we won’t be paying as much for products as in, say, 2019. Simply put, real estate prices will not continue to rise for some time, but they will not fall sharply.

It is also important to remember that property prices in the UK are heavily influenced by various assistance programs. Last year we wrote about the end of the Help to Buy program, which was very popular among our clients. The absence of HTB has certainly caused some potential buyers to abandon their plans to own their own home for a while, and these people are still not ready to move.

On the other hand, the demand for new properties has risen thanks to no down payment mortgages. Although not everyone will get one, it has certainly influenced the general interest in buying one’s own four walls.

To summarise: real estate prices may continue to fall, but I personally do not foresee drastic declines. Of course, this is just my opinion and literally anything can happen in the market. It does not change the fact that** it is worth considering a move in the coming months**.

And what has been happening in the UK property market over the past years and months?

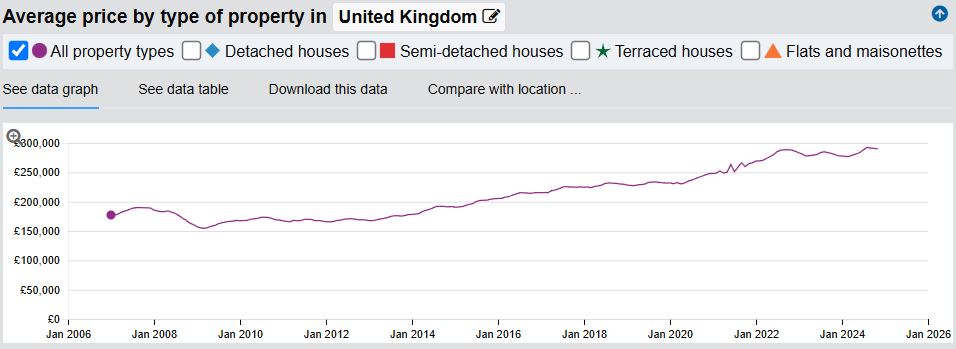

Property prices expressed in pounds are now really high. The last year in which we saw clear declines was 2008, while the last wave of increases actually lasted from 2009 to 2024! In the chart below, of course, you can see some slumps and moments of higher growth. It’s worth noting that the temporary reduction in the Stamp Duty fee was responsible for the sharp increase in the number of transactions in mid-2021 - it was simply that buyers wanted to complete their purchase as quickly as possible to save on tax.

This trend must eventually break down - real estate prices can’t keep rising without interruption.

UK property prices between 2007 and 2024

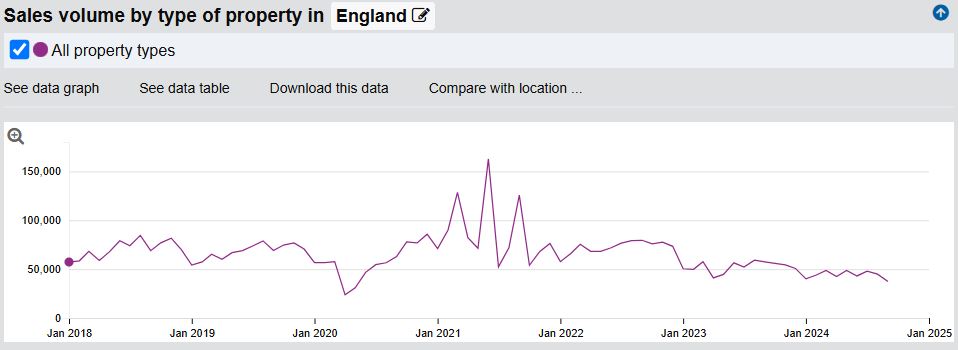

Very interesting developments have taken place in terms of the number of transactions. According to HMRC’s data, the beginning of the pandemic marked a huge stagnation in the real estate market, which then resulted in a clear rebound in mid-2021. Compared to April 2023, we once again see a clear recovery - the volume increased by 10%, as 90,430 houses, apartments and plots were sold in this month. All indications are that buyers have begun to take advantage of the rather attractive real estate prices, whose increments are less than inflation.

Monthly transaction volumes for 2018-2024

Nor should we forget the policies of banks, including the Bank of England. 2022 and 2023 passed us by with continuous interest rate hikes - the first of which took place on December 17, 2021, and at that time, meant an increase in the base interest rate from 0.1% to 0.25%. Today, i.e. January 15, 2025, the benchmark interest rate is already 4.75%, and this level has been in place for 2 months. The change from 5% to the current 4.75% in November 2024 was the first to lower the benchmark interest rate. It reached its highest value from August 2023 to November 2024, at 5.25%.

UK property prices expressed in various indices

In addition to the official UK House Price Index, there are several other equally useful indices. Certainly the reports provided by Rightmove are a good tool, but it is important to remember that they are based on offer prices, not transaction prices. Nationwide and Halifax also publish monthly summaries, but these are based on mortgage lending amounts.

Index Month-on-month change Year-on-year change Rightmove (December 2024) -1.7% 1.4% Nationwide (December 2024) 0.7% 4.7% Halifax (December 2024) -0.2% 3.3% Changes in UK house prices across several indices

Where do the differences come from? One of the conclusions we can draw from the table above is that sellers are more willing to negotiate, after all, offer prices have increased while tansaction prices have not. The differences between Halifax and Nationwide could be due to differences in their offers, for example.

Is the UK real estate market accelerating?

Some data and the general economic situation in the UK indicate it, but let’s not forget that there is a relatively small supply of properties for sale in the UK with high demand. This fact means that properties put up for sale, despite high prices, always find buyers.

The increasing number of properties on display, gently rising prices and the absence of violent geopolitical events may keep the UK housing market on a fairly similar level. Due to expensive mortgages, rapid increases in house prices in the UK are not expected, but the number of transactions should gradually increase.

What will happen with property prices in the rest of 2025?

Experts predict that real estate prices will rise, by up to 5%. The main recovery may come after the holiday season, that is, in September and October. This is typical, because customarily, the secondary market experiences a gentle slump during the holiday months, as does the stock market.

It’s worth remembering, however, that forecasts can be wrong-just three years ago, it was assumed that annual price growth would reach 5%, while in fact it was reported to be almost twice as high. Source: Rightmove forecasts house prices to rise nationally by 5% in 2022, and by 3% in London. Interestingly, Zoopla predicted even smaller increases, at 3%. Source: Zoopla - Housing Market in 2022.

On the other hand, forecasts for 2024 were extremely pessimistic, while instead of declines, we saw symbolic price increases. Of course, this does not mean that we should disregard analysts and specialists, but we recommend far-reaching caution. None of us can predict the future.

Is now a good time to buy property in the UK?

This question comes up really often, which is hardly surprising. No one will give you a definitive answer to this question, but it is worthwhile for you to consider a few particularly relevant facts:

1. Mortgages with low deposits are still available

In the Q&A we wrote that you only need a 5% deposit to get a mortgage. While this is certainly a large amount, especially for young people, raising several thousand pounds is realistic for many of us, especially on a yearly basis. Of course, the terms of a mortgage with an LTV of 95% will not be very attractive, but after a few years you can do a remortgage, moving to a potentially lower interest rate.

2. Stamp Duty Land Tax returns to previous rates

A package of changes to Stamp Duty Land Tax in England and Northern Ireland is planned to come into effect in April 2025. Particular interest is the change to the first tax threshold - from £250,000 to £125,000. The amount of relief will also change. Currently, first-time home buyers are exempt from paying SDLT on properties up to a value of £425,000. From 1 April 2025, this threshold will be reduced to £300,000 and the maximum value of a property qualifying for relief will be reduced to £500,000.

3. Interest rates are not likely to rise further

Recent months have shown that the series of interest rate hikes that the Bank of England has carried out throughout 2021, 2022 and 2023 have had the desired effect - inflation is now under control and remains at a very comfortable 2-2.5%. Unless anything changes, we can even expect further interest rate cuts, which will instantly encourage many families to buy their dream four walls.

4. House prices unlikely to fall markedly

There is little evidence of a marked slump in the property market. Just a few months ago, there were many reports of an impending recession or even crisis, whereas now there is only talk of an economic slowdown. Yes, the economic situation is not the best, but it can hardly be said to be really bad, so we do not expect drastic changes. Many even say that good times have returned to the market, and the global economy is doing quite well.

5. Rents are still increasing

Last year was marked by regular rent increases - they followed investment loan installments and property prices, which were, after all, getting more expensive. Although landlords have raised rents by relatively acceptable amounts, renting an apartment on the islands is still a fairly unprofitable option, and any interest rate cuts will make life easier for borrowers, not renters - those certainly won’t pay less than before.

Whether real estate prices are falling or not, if you are considering a purchase, you are cordially invited to a consultation. Our credit counselors will not only check your current creditworthiness and select the right product for your needs, but also answer all your burning questions. And if you found this post interesting, why not share it with your friends or sign up for our newsletter to receive information about our new articles?

FAQ

Frequently asked questions

How do we know what current property prices are?

Let’s start with some basic facts.

Where else can we get data from?

For more localised analysis, we can use ad portals like Rightmoveand Zoopla.

Will UK property prices fall?

In the previous paragraph I mentioned that real estate prices are gently lower than in previous months.

And what has been happening in the UK property market over the past years and months?

Property prices expressed in pounds are now really high.

UK property prices expressed in various indices?

In addition to the official UK House Price Index, there are several other equally useful indices.