TL;DR

In short

- Loan to value, popularly shortened to LTV, is the ratio of the value of the loan to its collateral.

- From a personal finance standpoint, you will encounter this term primarily in the context of mortgages, as it refers to the value of the property that serves as collateral for the bank.

- In most cases, we look at LTV from a slightly different perspective than we should we pay attention to the amount of the deposit (5%, 10%, 20%), but on the bright side, the bank is not interested in your cash.

- The standard range is 90 to 95 percent.

- Although such a question arises relatively rarely, from time to time we analyze with our clients whether it is worth paying a higher down payment.

LTV, or loan-to-value ratio, is mentioned in almost every article on mortgages. It’s hardly surprising - this ratio has a huge impact on the interest rate, and therefore the real profit of the bank financing your home. So let’s find out what exactly the mentioned LTV is and how to use its amount for your own purposes.

What is Loan-to-value ratio?

Loan to value, popularly shortened to LTV, is the ratio of the value of the loan to its collateral. As a rule, for consumer mortgages, this ratio is between 40 and 95% at the conclusion of the contract and, as subsequent installments are paid, it decreases.

With what kind of loans does the Loan-to-value ratio occur?

From a personal finance standpoint, you will encounter this term primarily in the context of mortgages, as it refers to the value of the property that serves as collateral for the bank. Loan-to-value will be extremely important for second charge mortgages, but if you go to pawn something to a pawn shop, this parameter will also determine your “creditworthiness.”

How does LTV ratio affects deposit?

In most cases, we look at LTV from a slightly different perspective than we should - we pay attention to the amount of the deposit (5%, 10%, 20%), but on the bright side, the bank is not interested in your cash. In the UK, it’s the ratio of the loan amount to the value of the property that matters, and for this reason, if an appraiser valued the property you were buying at, say, 20% above the transaction price, you would be able to borrow 100% of the amount needed to complete the transaction.

How much is the LTV of mortgages in the UK?

The standard range is 90 to 95 percent. However, many banks offer a much wider range of offers - products with LTVs of 85 percent, 80 percent, 70 percent and even 40 percent are available. On the whole, the lower the loan-to-value ratio, the better.

However, it can happen that the LTV exceeds 100% - this happens when the valuation of your property drastically decreases, for example, as a result of a financial crisis, unfavorable changes in the immediate environment or even a fire. Add, however, that such a phenomenon is extremely rare - among other things, this is why conveyancing is performed, during which your lawyer will ascertain the zoning plan or possible road investments in the immediate vicinity of your future home.

What LTV should my mortgage have?

Although such a question arises relatively rarely, from time to time we analyze with our clients whether it is worth paying a higher down-payment. Unfortunately, answering it is not so easy.

Consider the first case:

Martha and Jacob want to buy a house worth £250,000 with a 25-year mortgage. They have savings of 30 thousand and are looking for financing with a fixed interest rate for 2 years. A loan advisor from HSBC bank has offered them 2 deals - with an LTV of 95% at 5.89% per year and with an LTV of 90% at 5.28% per year. Which should they choose?

In the former case, that is, with a deposit of 5% (£12,500), the loan installment would be £1514.29, while with an LTV of 10% (£25,000), it would drop to £1,352.29. If Martha and Jacob wanted to get an equally attractive installment with a deposit limited to 5%, they would have to repay their home over 28 instead of 25 years. Nonetheless, with identical terms, a 10% deposit yields a £162 lower installment, which over the 2-year term of the preferential loan agreement means as much as £3888 in savings.

Let’s also analyze another situation:

Andrew and Michael want to buy a large apartment worth £400,000, also using a mortgage. This time, however, the story’s protagonists would like to pay off their commitment in just 10 years, and can afford as much as a £150,000 contribution from the sale of their previous apartment. Andrew is afraid of risk, so when looking for a mortgage, he leans toward offers with a long, as much as 5-year fixed rate period.

This is, of course, a very rare example - in order to be able to repay such a mortgage, applicants would have to show a very high income, and in this day and age, choosing a fixed-for-5-year product is not advisable, but this story should give you a better understanding of the whole problem with LTV and gradation of mortgage offers. In this case, HSBC bank could offer a mortgage with an LTV of 60% or 70% with interest rates of 4.14% and 4.37% respectively. This, in turn, would translate into £2,445.88 or £2,884.36, which would have to be transferred to the bank every month.

Is the higher the deposit the better?

We can probably agree that as the deposit increases, the installment decreases - this is perfectly normal, after all, the amount borrowed is smaller and the bank takes less risk. On the other hand, the second example shows that in some cases you have to make a much larger deposit (160 instead of 120 thousand) to save just a little - 0.23 percentage points is just £230 less interest on every hundred thousand borrowed per year.

The offers of the vast majority of banks are structured in such a way that it doesn’t pay to make more than a 30% equity contribution - you’ll see real differences in interest rates between loans with LTVs of 95% and 90%, but no longer necessarily between 60% and 70%. In other words, committing an extra chunk of cash basically always translates into a lower interest rate, but sometimes it’s not worth it. How is this possible?

It’s all about time, of course. By putting aside an extra £10-15 thousand you will spend the next few months renting an apartment instead of enjoying your own home. Assuming you’re leaving your landlord around £15,000 in rent per year, it’s sometimes better to opt for a slightly more expensive mortgage, and when the opportunity strikes, you’ll be able to remortgage or make an overpayment after all.

Is it worth taking a mortgage with an LTV of 95%?

In our opinion, as much as possible! Let’s go back for a moment to the example of Martha and Jakub, who received an offer has 5.89% per year.

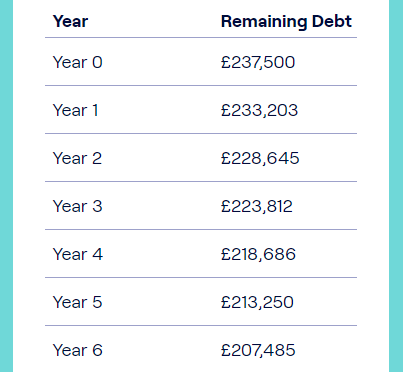

A mortgage calculator from the Moneyhelper website indicates that those paying off a £237,500 loan for 25 years will have already repaid £13,688 of principal after 2 full years, so there is a very good chance that the LTV ratio of their mortgage will fall below the 90% barrier. This is illustrated in the table below:

If the terms of the mortgage agreement are submitted in this way, the protagonists of our example should remortgage, that is, refinance their mortgage. For another bank, Martha and Jakub will be attractive customers, whose own contribution exceeds 10%, which will make them a much better offer. Interestingly, if interest rates and bank offers remain unchanged for the next 2 years, the installment on the new mortgage would be about £110 lower. Alternatively, remortgaging and lowering interest rates could lead to a shorter mortgage term by as much as 3 years!

As we’ve already mentioned, postponing the decision to move isn’t good - every month of delay means hundreds of more pounds you’ll spend on renting someone else’s property instead of paying off yours. For the first few years, a mortgage may be the more expensive option, but in just a few years the situation will change.

Summary

Mortgages are our specialty - we have been dealing with them for many years and make sure that our clients get only the best deals from both international and local banks. So if you are planning to buy a property and are looking for the best mortgage advisor who will explain every detail of your future deal in simple terms, don’t hesitate - Extend Finance will be an excellent choice.

FAQ

Frequently asked questions

What is Loan-to-value ratio?

Loan to value, popularly shortened to LTV, is the ratio of the value of the loan to its collateral.

With what kind of loans does the Loan-to-value ratio occur?

From a personal finance standpoint, you will encounter this term primarily in the context of mortgages, as it refers to the value of the property that serves as collateral for the bank.

How does LTV ratio affects deposit?

In most cases, we look at LTV from a slightly different perspective than we should we pay attention to the amount of the deposit (5%, 10%, 20%), but on the bright side, the bank is not interested in your cash.

How much is the LTV of mortgages in the UK?

The standard range is 90 to 95 percent.

What LTV should my mortgage have?

Although such a question arises relatively rarely, from time to time we analyze with our clients whether it is worth paying a higher down payment.