TL;DR

In short

- As we have written in the past, a credit score is a point rating of your reliability as a borrower.

- There are several ways to do this, but for several years we have been recommending checkmyfile as the platform of choice for our clients.

- Let’s now take a look at the sample report we made for this article.

- In simplest terms, you should do exactly the opposite of what Jan Kowalski did in our example.

As a large proportion of banks charge a fee for applying for a mortgage, it is worth preparing yourself well for such a process - a negative decision will simply mean losing a certain amount of money and will add a lot of stress to you. While the final say on the matter always rests with the risk assessment analyst, your credit score is also of considerable importance. That is why, in this article, we will analyse this issue and find out how to know the exact value of this indicator in your situation.

What is a credit score?

As we have written in the past, a credit score is a point rating of your reliability as a borrower. On a scale of 0 to 999, credit scoring agencies try to express how you have performed so far in terms of giving back money and how reliable a customer you will be for your bank. The higher your credit score, the easier it will be for you to get a loan, lease or any kind of credit.

How do you check your credit score?

There are several ways to do this, but for several years we have been recommending checkmyfile as the platform of choice for our clients. Frankly speaking, its biggest advantage is simply value for money - access to results is free for the first 30 days, which in many cases is completely sufficient.

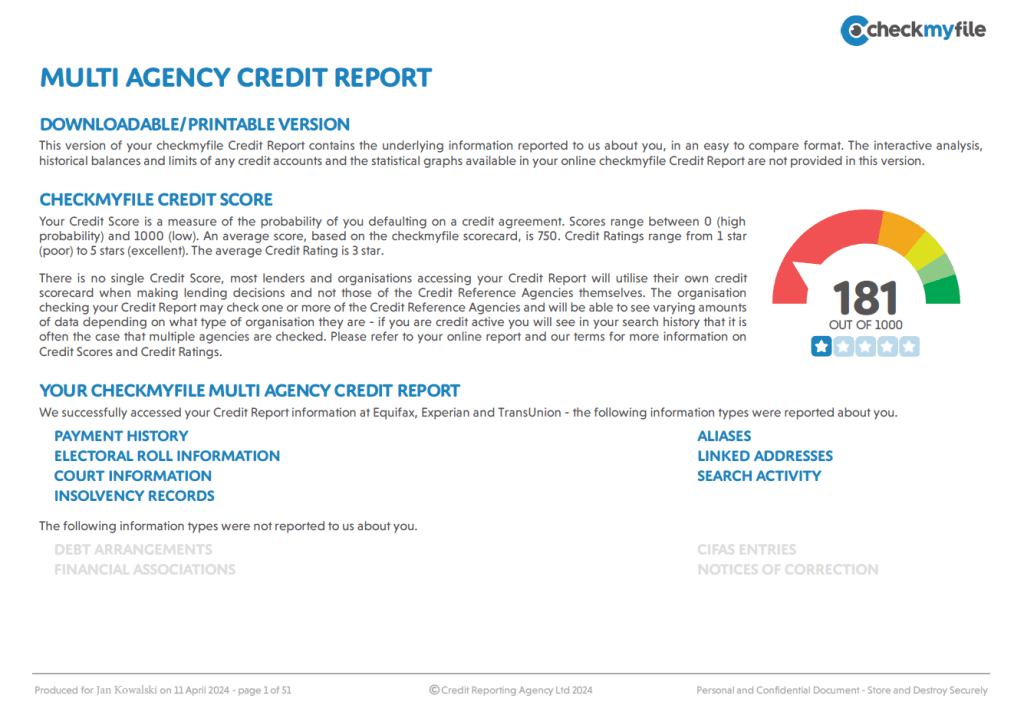

What does a checkmyfile report look like?

Let’s now take a look at the sample report we made for this article. We hope that it will give you a slightly better understanding of how the programme itself works. In this hypothetical example, the borrower is Jan Kowalski, who is 30 years old.

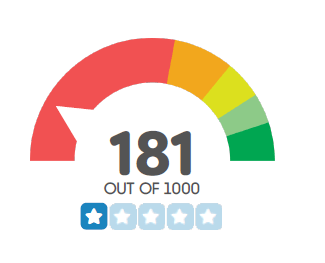

Each credit report contains essentially the most important piece of information - your credit score

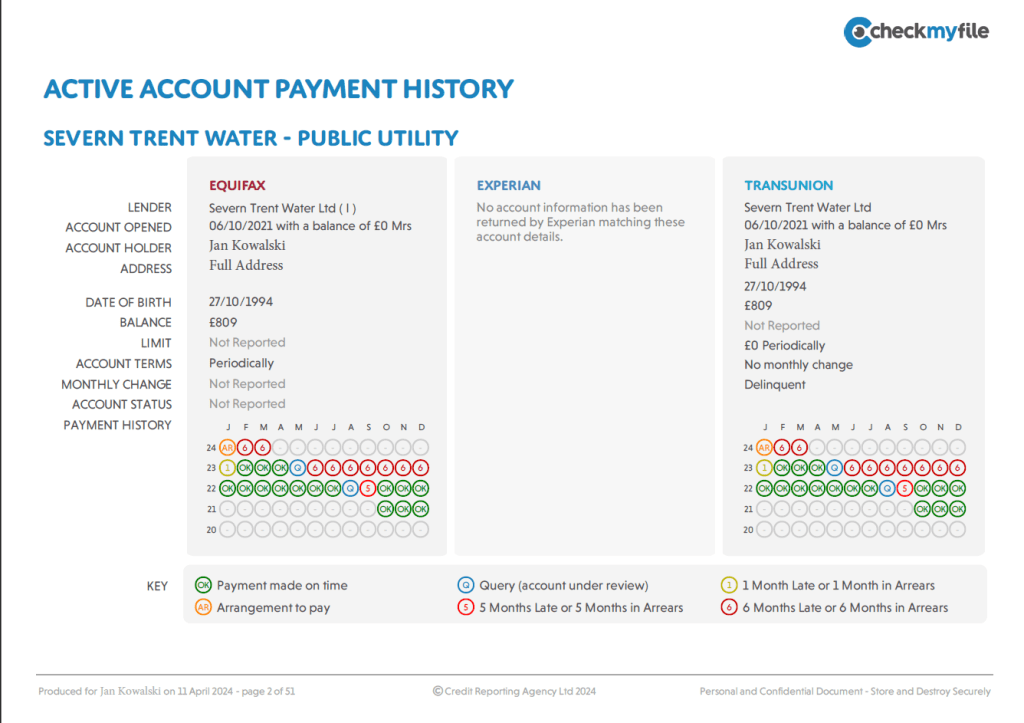

Arrears in payment of obligations

As can be seen from the illustration above, the protagonist of our sample report has had serious problems in the past with paying his obligations. In the case of water supply charges, there were even six-month delays! It matters little that the arrears amounts were probably low - in the eyes of the bank, our example Jan Kowalski is simply unreliable.

However, let us point out that mistakes can occur in this part of the report and it is not all that unheard of. Before you start submitting documents to the bank, it is important to make sure that there is no mistake and that your electricity, water, gas or internet provider has not simply provided incorrect information. You may find that your credit score will increase significantly with virtually no sacrifice on your part.

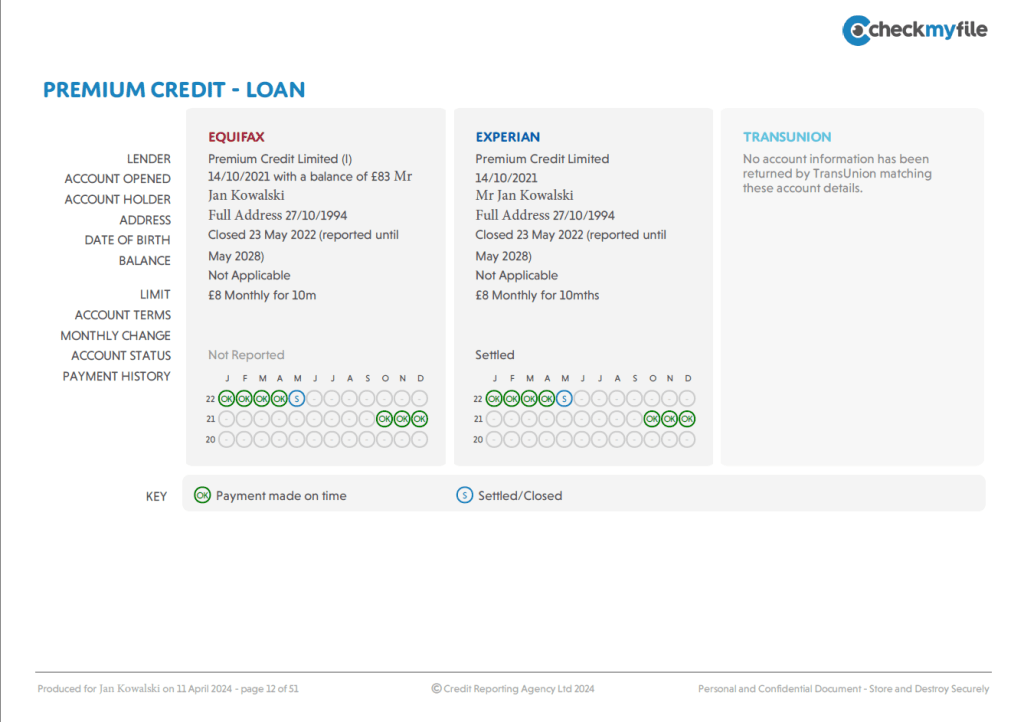

Correct payment history

There are also parts of the report where our Jan Kowalski performs very well. On the attached image you can see a summary of the loan, which the protagonist of this article has been paying for 8 months. As you can see, each instalment was paid on time, which certainly has a positive impact on the credit score. We should add that the report shows that the commitment was repaid in May 2022 - this is symbolised by the letter S in a circle.

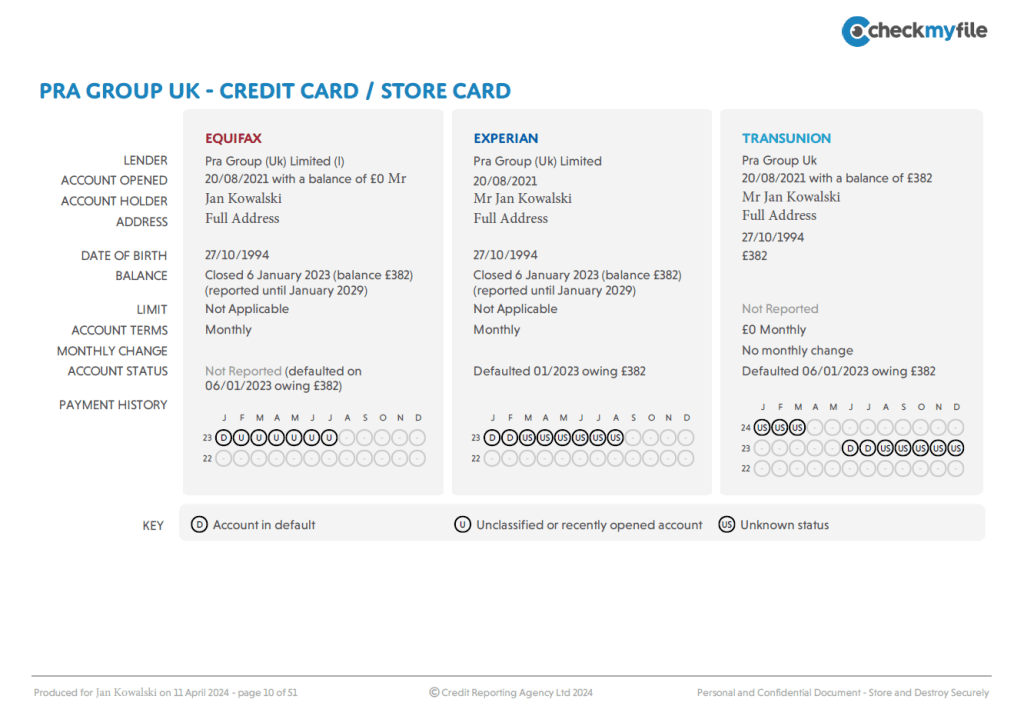

Unknown status of financial product

Reviewing our sample credit report, we finally arrive at credit cards. As is well known, buying on instalments affects your creditworthiness in the UK in two ways - timely repayments improve your credit score, while the total value of your credit limits reduces your creditworthiness. For this reason, it is very important that you use one, maximum two cards.

In the illustration above, you may notice that the payment status has been marked as ‘unclassified’ and ‘unknown status’. Most likely, our applicant was not using his card, or, as is also likely, was paying off his debts very quickly. Either way, the credit card was unlikely to have had a negative impact on this person’s history, and its deactivation in January 2023 had a positive impact on this person’s creditworthiness.

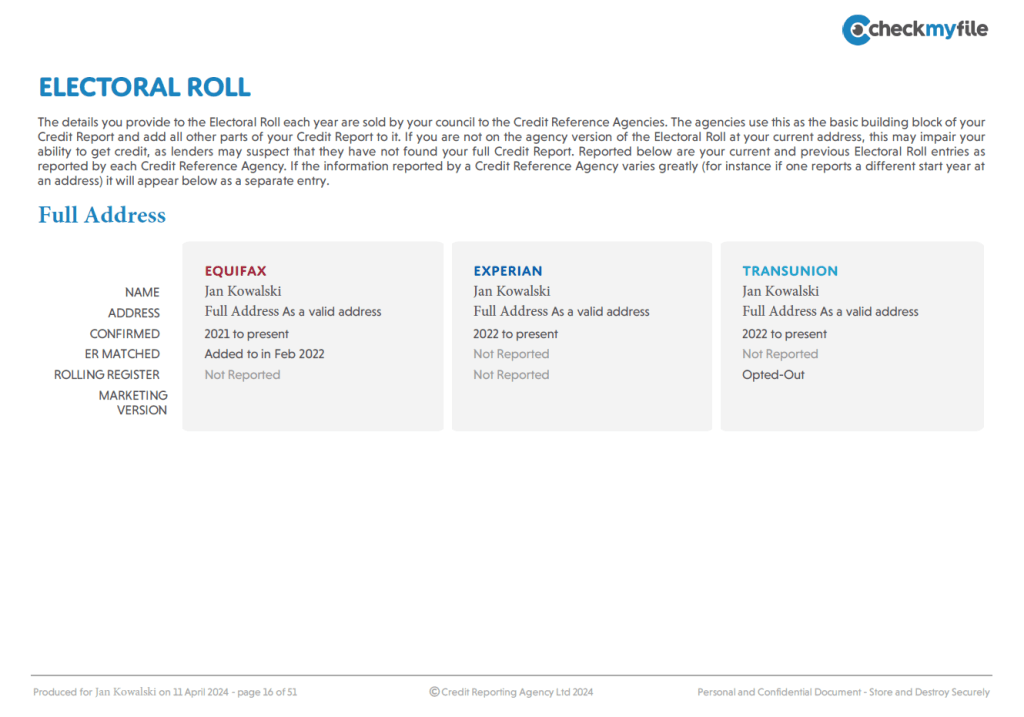

Register of electors

When taking out a mortgage you should remember that a great way to improve your credit score is to sign up to the electoral roll. For credit rating agencies and lenders, your presence on the electoral roll is a signal of your ties to the local community, which is generally positive news.

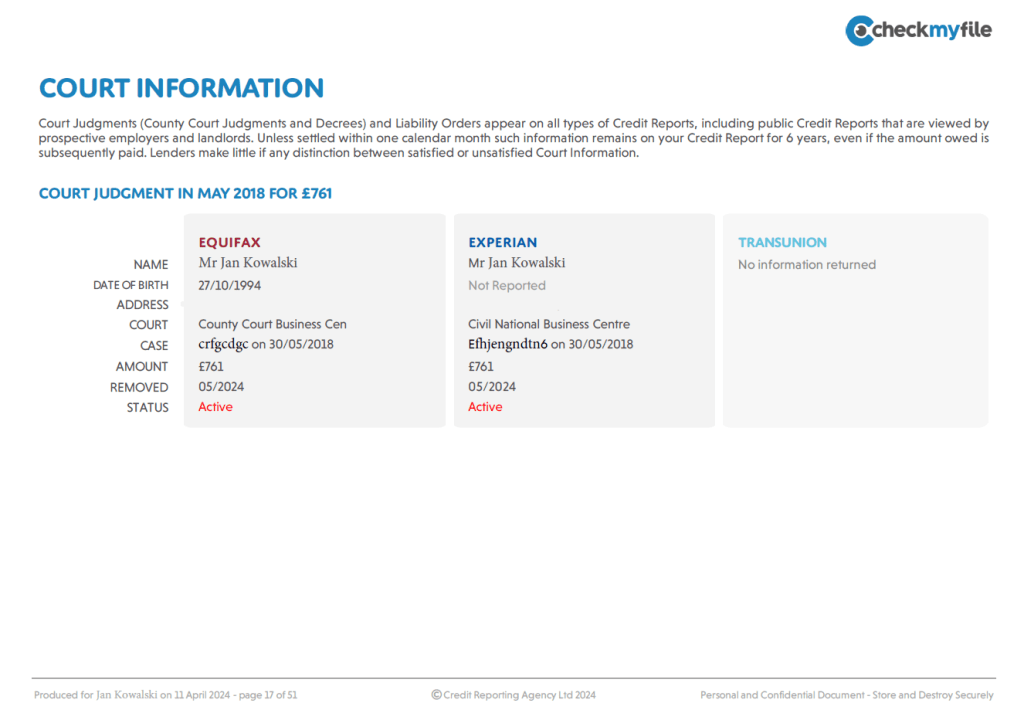

Court judgments

Unfortunately, the hero of our example gets into trouble quite often. According to the report, in May 2018, during a hearing, he was ordered to pay £761, which he has so far still not complied with. As you can easily guess, the six-year delay in regulating the obligation has a downright fatal effect on Jan Kowalski’s credibility in the eyes of the banks and is one of the main reasons for his currently low credit score - as a reminder, Jan received only 181 points out of a possible 1,000.

As a consolation, we can add that the record will disappear at the end of May, which should reflect positively on the credit score. Differences in scores can reach up to 100 points, so it is definitely worth waiting :)

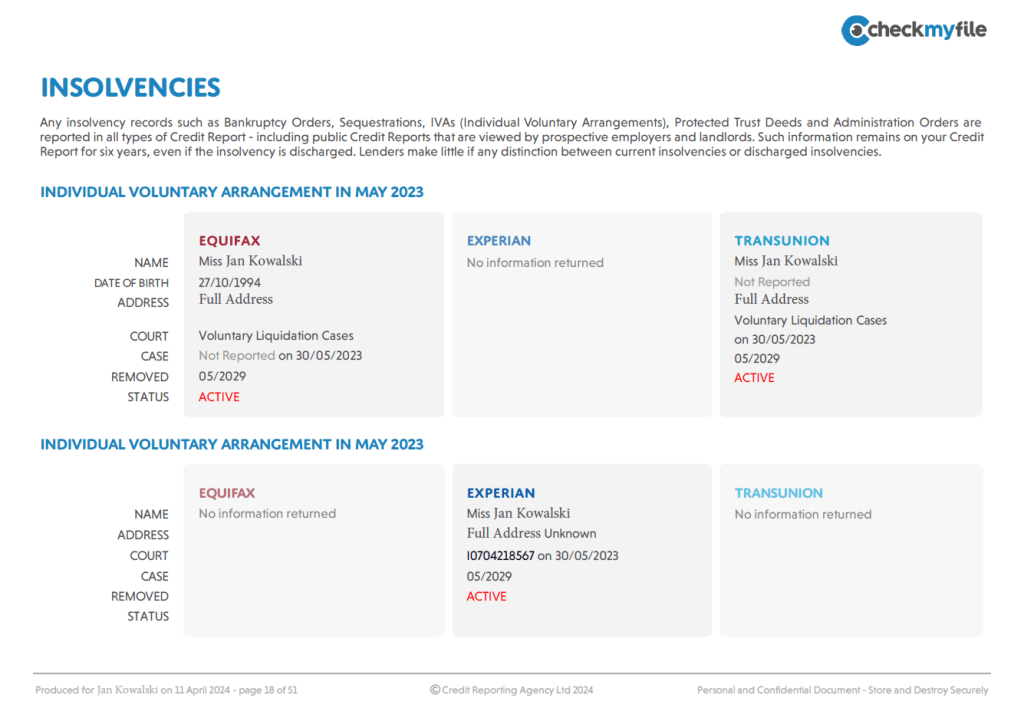

History of bankruptcies

Unfortunately, there is also an event on Jan Kowalski’s credit report that makes it essentially impossible for him to obtain a mortgage. Bankruptcy, or a state of complete insolvency, is an extremely undesirable situation for any rational lender. Simply put, a person who decides to settle financially is treated as someone who is unable to make responsible financial decisions.

Of course, if our hypothetical Jan Kowalski had declared bankruptcy 2-3 years ago and since then had done everything possible to improve his financial situation, there is a shadow of a chance of obtaining a loan. However, these are rare situations and, in the history of our company, we have seen only a few cases in which it would be possible to find a bank willing to provide financing in such a situation.

Credit applications

Unfortunately, the report we analysed also contains a large number of credit applications. Regardless of whether Jan Kowalski received loans or not, the rating agencies recorded his attempts, of which there were as many as 10 in the last two years. This is a very large number and we can assume with a high degree of probability that each of them, gently downgraded our borrower’s rating.

Let us note at the same time that events from May and June 2023 appear in the report, i.e. just after Jan Kowalski declared his insolvency. As you can guess, banks were unlikely to decide to grant loans, and even if they issued positive decisions, the interest rates on such products were certainly not low.

Soft credit checks

The solution that every person thinking about a mortgage should choose is the so-called soft credit check. In simple terms, this is the procedure of checking your credit score without affecting it. For the credit rating agencies, such an event simply means that you want to check your credibility without attempting to borrow funds. The report shows that an insurance company as well as a credit card bank, among others, have decided on such a move.

What should I do to raise my credit score?

In simplest terms, you should do exactly the opposite of what Jan Kowalski did in our example.

First and foremost, you should absolutely protect yourself from getting into financial difficulties that could lead to your bankruptcy. We know that driving a new car, owning the latest phone and taking a foreign holiday provide plenty of pleasure and you need to spend a lot of money to enjoy them, but going into debt to do so is very risky. Think for yourself - do you have a guarantee that your income over the next three years will definitely not fall? Well, that’s right, nobody has.

Also try to limit the number of financial products and subscriptions. We know that borrowing money is tempting and there are no exceptions to this rule - everyone wants to live beyond their means. However, remember that the more instalments you pay, the greater the risk that you will forget one of them, and this, too, has a very bad impact on your credibility as a borrower.

Finally, you should seriously think about raising a certain amount of money for a black hour. Even a small financial reserve of £3,000 or £4,000 will help you greatly in building your financial security.

FAQ

Frequently asked questions

What is a credit score?

As we have written in the past, a credit score is a point rating of your reliability as a borrower.

How do you check your credit score?

There are several ways to do this, but for several years we have been recommending checkmyfile as the platform of choice for our clients.

What does a checkmyfile report look like?

Let’s now take a look at the sample report we made for this article.

What should I do to raise my credit score?

In simplest terms, you should do exactly the opposite of what Jan Kowalski did in our example.

What should I know?

The key details are explained in the article above. If you are unsure, it is worth speaking with an adviser before making a decision.