In the UK, the rules regarding property insurance are relatively strict. Insurers scrutinise every application in detail for any inaccuracies that might increase the premium or prevent them from issuing a policy altogether – this is how they protect themselves against excessive risk. Before you buy a home in the UK, it is a good idea to familiarise yourself with the realities of the insurance market and find out which properties or their features you should avoid.

TL;DR

In short

- UK insurers can reject a home insurance application when the property or the applicant creates a higher risk.

- Building insurance covers the structure of the property and is normally required when the home is mortgaged.

- Non-standard construction, listed status, flood risk or subsidence history can make buildings insurance difficult or impossible.

- Poor security, a high-crime postcode or living with flatmates can affect contents insurance.

- Previous insurance problems, claims history, criminal convictions or bankruptcy can also limit access to cover.

How does home insurance work in the UK?

In the UK, home insurance is divided into two main categories. The first is standard building insurance. This type of policy covers only the fixed structures of the property, not the contents inside it. This includes walls, the roof, doors, windows, and so on.

The cover is mainly focused on natural hazards such as floods or hurricanes – for example, if a storm damages the roof, you will be able to claim compensation. On the other hand, if someone breaks into your home and steals a television, the insurance payout will only cover the cost of a broken door lock or a smashed window.

It is worth remembering that building insurance is always required if the property is subject to a mortgage.

The second pillar is contents insurance. This policy does not protect the building itself, but focuses on the items inside. In a similar situation, if a thief were to break into the house by damaging the door lock and steal the television, contents insurance would cover the cost of a new television, not the damaged lock.

In practice, these two types of insurance are usually sold as a package. Even if you don’t have a mortgage, it is strongly recommended that you take out both policies – you never know what might happen to your home, and both water damage and burglary are fairly common problems in the UK. It is worth noting, moreover, that a well-chosen, comprehensive home insurance policy is affordable.

In this post, we will give you an overview of the situations in which an insurer may refuse to issue a policy. If you are looking for a property in the UK, this knowledge will help you avoid choosing a home that cannot be insured.

Building insurance

There are situations in which an insurer refuses to provide a building insurance policy. This is usually due to the high likelihood that the house will suffer damage and that compensation will need to be paid out quickly.

Unusual house construction

If the building you have chosen has an unusual construction, it may be difficult to insure. This is because most insurers prefer ‘ordinary’ houses, built in the standard way, known as standard construction. This means brick or stone walls and tiles or slate on the roof. Any other construction method is treated as “non-standard construction”, which to an insurer simply means “risky”. As a rule, a non-standard house design in the UK also makes it impossible to obtain a mortgage.

One of the most problematic factors is a non-standard roof. This could be, for example, a flat roof, which is far more susceptible to damage and water retention. If it accounts for more than 30–40% of the total surface area of the house, most insurance companies will reject the application. Another example is thatched roofs, which are highly susceptible to fire. Because of this, many insurers automatically reject the application, and those willing to consider it often require chimney and electrical certificates every 2–3 years.

Another example of non-standard constructions is prefabricated houses. In recent years, many modern construction methods have emerged on the market that lack a documented history which could demonstrate to insurers how a house behaves under various circumstances. These methods are also little known to the surveyors who value the property and assess the risk. All this means that insurers are very reluctant to insure houses with non-standard construction.

This problem does not only concern modern construction methods – in the UK there are many old houses that were built in the 1950s and 1960s using prefabricated concrete blocks. Years later, it turned out that the steel reinforcement inside the concrete was corroding, meaning that many of these buildings were deemed structurally unsound. If a house has not undergone a certified repair (PRC Repair Scheme), insuring it is virtually impossible, and the bank will not grant a mortgage for it.

Listed building

Occasionally, a house listed on the UK’s heritage register is put up for sale. In such cases, there is one important legal detail that may mean insurers are unwilling to insure the property. This refers to the obligation to rebuild the house using the exact same methods and materials as were originally used, should it be destroyed. This entails enormous costs that no standard policy will cover. Insurance for a listed building is often 3–4 times more expensive.

The location and its history

A key factor in assessing an insurance application is the location of the property in question. Any documented hazard increases the risk and reduces your chances of securing an insurance policy on favourable terms. Two main factors are taken into account:

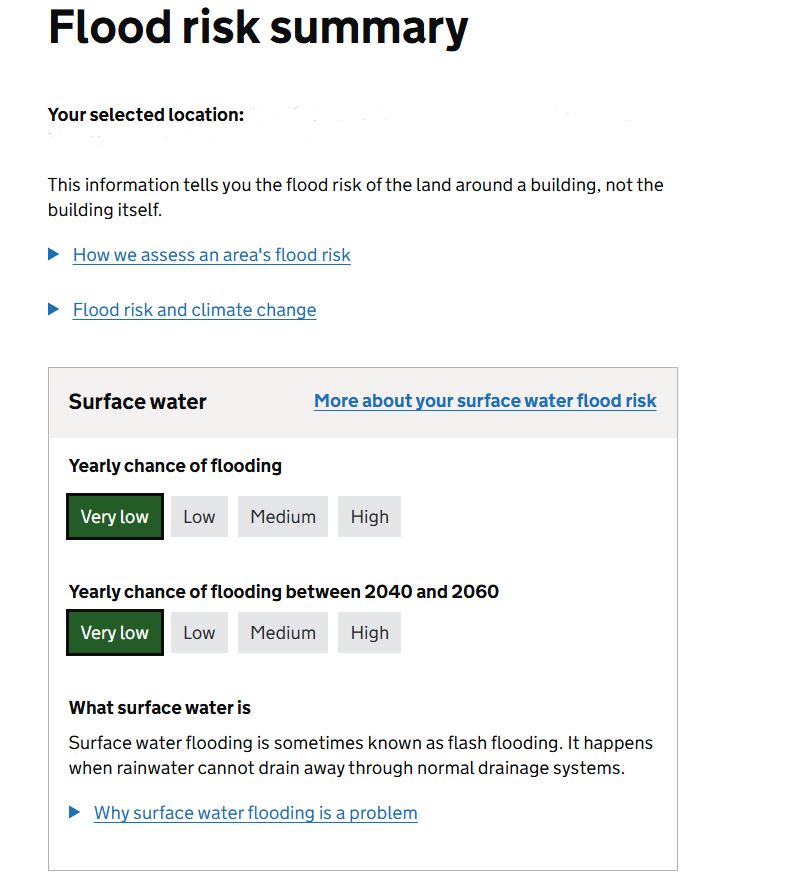

Firstly – flood risk. This is a serious problem across the UK and has a significant impact on the insurability of buildings. Statistics show that over 6 million properties are at risk of flooding, which accounts for around 20% of all properties in the UK. If the house you have chosen is located in a high-risk area, you may face significant difficulties in insuring the property. Given the scale of the problem, the government has developed a special online tool that allows you to easily check the level of risk associated with a particular address.

The second factor that insurers take into account is building settlement. If a property has even a single historical instance of settlement on its records, most standard insurers will refuse cover. This is because even a single instance of building settlement indicates that the soil is prone to excessive movement, meaning that it could happen again in the future. This fact is sufficient grounds for an insurer to increase the premium or even refuse cover altogether.

Contents insurance

In the case of contents insurance, the situation is slightly different. As it primarily protects against theft, the key requirements mainly involve adequately securing your home and your belongings. Insurers operate on the assumption that they cannot cover property that is inadequately protected.

This gives rise to requirements such as a front door with a five-lever mortice deadlock compliant with BS3621, windows with locks, or a working alarm.

Location also plays a significant role here – some neighbourhoods in larger UK cities have such high crime rates that, in the eyes of insurers, the risk increases dramatically. There have been instances where insurance companies have refused to insure a property or a car solely because the postcode falls within a so-called ‘black zone’, i.e. an area with a very high crime rate.

Living with flatmates

Insurers take a slightly different view of property insurance claims when you share a property with strangers. This is because they take into account the possibility of so-called ‘internal theft’, i.e. theft committed by a flatmate. A standard contents insurance policy will not apply in such cases, and you will need a policy known as tenant insurance – which also has its own requirements regarding the security of your belongings.

Factors unrelated to the property’s characteristics or location

You should be aware that your reputation with the insurer also influences the decision on your application and may make it difficult or completely impossible to obtain cover. There are several situations in which insurers reject an application not because of the property’s characteristics, but because of the customer themselves.

Blacklist

Information about how you have fulfilled your insurance contracts is entered into databases accessible to other insurance companies. So, if you have previously found yourself in a situation where an insurer has terminated a contract (e.g. because you stopped paying premiums) or refused to pay out a claim due to attempted fraud or negligence, you may be placed on a blacklist – a register of customers with whom insurance companies do not wish to work.

Please note that even if there is no record of this in the databases and you do not mention it on the claim form, this constitutes fraud, which will prevent you from receiving compensation.

Claims history

Another factor that could put you at a disadvantage is your claims history. If you have made claims in the last 3–5 years (even for minor thefts or water damage), you will be considered a ‘high-risk’ customer. Unfortunately, insurers use such statistics and conclude that someone who has already made a claim is likely to do so again.

You should also bear in mind that if you have an open claim, most companies will not issue a new policy until the old claim has been formally closed.

Criminal history

Under UK law, you must disclose any unexpunged criminal convictions when applying for cover. This applies to all members of the household, not just the policyholder. So if you or a member of your family has been convicted of theft, fraud or arson, your application will almost certainly be rejected. Even if the conviction is not property-related (e.g. for a fight), it may lead the company to consider you untrustworthy.

Here too, if you fail to disclose any convictions when applying, you will be committing an offence.

Financial status

If you have declared personal bankruptcy or have a history of debt-related convictions, the insurer may refuse to sell you a policy on instalments, and sometimes refuse cover altogether, due to concerns that you will not look after the property due to a lack of funds.

Summary

There are several reasons why an insurer may increase premiums or even refuse to issue a policy. These include:

- Property characteristics;

- Location;

- The policyholder’s profile.

Remember to bear these in mind when choosing a home to avoid disappointment. If you are unsure about the property you have chosen, please contact us – our insurance advisers are always ready to help.

FAQ

Frequently asked questions

Can an insurer refuse to insure a home in the UK?

Yes. An insurer may refuse cover if the property has high-risk features, such as non-standard construction, flood exposure, subsidence history or serious security issues.

Is building insurance required with a mortgage?

In most cases, yes. If the property is bought with a mortgage, the lender usually requires buildings insurance to protect the structure of the home.

Can a non-standard property be difficult to insure?

Yes. Flat roofs, thatched roofs, prefabricated buildings and some older concrete constructions can be treated as higher risk by insurers.

Does location affect home insurance?

Yes. Flood risk, subsidence history and high crime rates in the postcode can increase premiums or make some insurers refuse cover.

Can my personal history affect a home insurance application?

Yes. Previous refused claims, unpaid premiums, recent claims, unspent criminal convictions or bankruptcy can all affect whether an insurer offers cover.