TL;DR

In short

- The expression ‘interest rate’ is not entirely precise a better term is rather ‘reference rate’ or ‘base rate’.

- To understand the impact of interest rates on mortgage repayments, let us start by presenting a simple formula: Where: EMI repayment amount P amount of credit granted (principal) This article is not about mathematics, so let us now draw…

- The vast majority of mortgages in the UK are provided at a fixed rate, which is locked in for a period of between 2 and 5 years.

- This is a question probably asked by everyone who is planning to buy a home in the UK in the coming months.

- To understand the impact of interest rates on mortgage repayments, let us start by presenting a simple formula:

As interest rates fall, mortgage rates offered by UK banks are starting to fall. However, as we’ve seen, many people don’t fully realise the impact that even a small change such as 0.25% or 0.5% has on their repayment. In this slightly more than usually mathematical blog, we’ll use some examples to help you understand how changes in interest rates affect mortgage repayments. We invite you to read on.

What is the interest rate?

The expression ‘interest rate’ is not entirely precise - a better term is rather ‘reference rate’ or ‘base rate’. Due to the universality of the phrase, however, we will use it. After all, the point is to convey the meaning, not to preserve dictionary precision.

As reported by the Bank of England, the interest rate is a percentage measure of the cost of borrowing money in the economy. As a rule of thumb, the more people want to take out a mortgage, the higher prices banks can offer them and, similarly, the less interest there is in borrowing, the cheaper it has to be to induce demand for such services.

More broadly, the interest rate is also a much-needed economic tool with which inflation is controlled. As interest rates rise, borrowing becomes more difficult and, as a consequence, demand is reduced and prices are lowered. However, this has its negative consequences, as reference rates that are too high can lead to an economic crisis.

How do interest rates translate into mortgage rates?

To understand the impact of interest rates on mortgage repayments, let us start by presenting a simple formula:

Where:

EMI - repayment amount

P - amount of credit granted (principal)

This article is not about mathematics, so let us now draw the most important conclusions from the above equation. Firstly, extending the repayment period drastically increases the total cost of repayment at the expense of an apparent reduction in the repayment. Extending your mortgage by a year or two can mean that, in total, you will pay back several hundred or even several thousand more to the bank.

Secondly, a small change in interest rates can affect the repayment very significantly. Let us illustrate this with an example:

Interest rate / credit term 20 years 25 years 30 years 1% £459.89 £376.87 £321.64 2% £505.88 £423.85 £369.62 3% £554.60 £474.21 £421.60 4% £605.98 £527.84 £477.42 The mortgage amount used for the example is £100,000 and the calculations were based on the formula above.

As you can easily see, a mortgage interest rate increase from 1% to 4% raises the repayment by around 40%! Consider, however, that the increase in mortgage repayments is not the only ailment resulting from interest rate rises. If you are just applying for a mortgage or planning to remortgage, you need to be aware of the decrease in your creditworthiness, which is derived from the maximum amount you can afford to pay each month. You can read more about this in our post on affordability.

What to do in the event of an interest rate rise?

The vast majority of mortgages in the UK are provided at a fixed rate, which is locked in for a period of between 2 and 5 years. By force, the fixed rate actually provides you with security for a while, but once the period of preferential rates ends, your repayment will already be calculated based on the current base rate. As a result, you will most likely end up suffering the financial consequences of the Bank of England’s decision. However, you can prepare for this.

Prepare your household budget for the extra burden

Higher repayments will catch up with you sooner or later and the better prepared you are for this, the less painful the changes will be.

Knowing about the interest rate rise, it is worth thinking about increasing your earnings - you have a higher income, you will be able to offset the increase in your expenses. It is also obvious to cut living costs, for example by terminating unnecessary subscriptions, saving electricity or planning your purchases more sensibly.

Proper management of your personal finances will help you take the next step, which is to save money.

Collect as much money as possible

The UK banking system is structured in such a way that overpaying on a mortgage doesn’t benefit you immediately - your repayment period decreases, but your repayments remain the same. As a result, when interest rates rise, you will have to pay more. Building up an adequate cash reserve will not only allow you to cover at least part of the difference in repayments, but will also help with the next point.

Change the bank

When your fixed-rate deal ends, the terms of your mortgage may not be favourable. In the vast majority of cases, you will even find that by changing banks and choosing a new deal you will be able to reduce your interest rate by 0.5% or even 0.8%. There are, of course, additional costs involved in carrying out a remortgage, such as a broker fee, and it takes time - there is no denying that. However, as our statistics show, remortgaging is a very worthwhile investment that typically pays for itself in just over nine months.

By doing a remortgage, you can extend the repayment period and therefore lower the repayment, shorten the term of the mortgage by paying the same amount or leave the repayment schedule identical but most likely pay less. In many cases, our clients are able to pay off their homes 2-3 years faster just by switching banks regularly using specialists.

Will UK interest rates fall in 2025?

This is a question probably asked by everyone who is planning to buy a home in the UK in the coming months. As an experienced UK mortgage adviser, we are unable to give you a categorical answer, but we can suggest some publicly available considerations.

UK inflation is already very low

Inflation in October 2024 was 3.2 per cent, which guarantees a stable level of price growth. The fundamental objective of raising interest rates has therefore been achieved - the market is no longer overheated and the cost of living for the British people is no longer rising as sharply as it was just two years ago.

Interest rates are being lowered worldwide

Interest rates are already being lowered in the United States and the European Union, and usually, this type of action is globally coordinated. In this case, however, it is not a sheepish rush - it is simply that central banks are adapting their policies to the actions taking place globally, not just in one country.

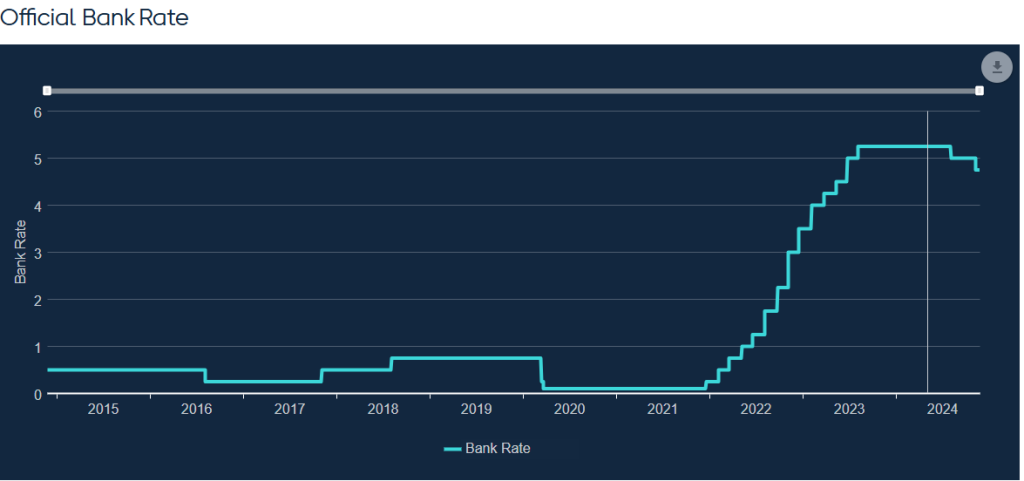

Current interest rates are very high

The official interest rate chart can be found at bankofengland.co.uk

The current level of interest rates is very high if we look at it from a historical perspective. Yes, mortgages in the UK used to be even more expensive, but the last decade has accustomed us to interest rates several times lower. The current situation in the property market is therefore a departure from the rule and the historical trend.

FAQ

Frequently asked questions

What is the interest rate?

The expression ‘interest rate’ is not entirely precise a better term is rather ‘reference rate’ or ‘base rate’.

How do interest rates translate into mortgage rates?

To understand the impact of interest rates on mortgage repayments, let us start by presenting a simple formula: Where: EMI repayment amount P amount of credit granted (principal) This article is not about mathematics, so let us now draw the most important conclusions from the above equation.

What to do in the event of an interest rate rise?

The vast majority of mortgages in the UK are provided at a fixed rate, which is locked in for a period of between 2 and 5 years.

Will UK interest rates fall in 2025?

This is a question probably asked by everyone who is planning to buy a home in the UK in the coming months.

What should I know?

The key details are explained in the article above. If you are unsure, it is worth speaking with an adviser before making a decision.