TL;DR

In short

- First of all, let’s look at probably the most important detail related to the purchase of a property, namely prices.

- If you have read the articles on our blog, you probably know that when you buy a house in England, you have to pay tax on the transaction.

- Unfortunately, from the first of April 2025, buying a home in Northern Ireland will become a tad less attractive, all thanks to the increase in Stamp Duty Land Tax that will take effect in April 2025.

- As with the transaction tax (SDLT), Northern Ireland’s assistance schemes are very similar to those in England.

- Some of our clients wonder whether buying a house pays off more than renting.

Most blogs on mortgages in the UK focus primarily on the realities in England and Wales, sometimes including Scotland. In order not to leave anyone without answers to their questions, we have decided to tackle the description of buying a home in Northern Ireland. From today’s article you will learn about, among other things:

-

Property prices in Northern Ireland in 2025;

-

The formalities involved in buying a house in Ireland;

-

Local regulations related to mortgages in this country;

We warmly invite you to read on.

How much does a house cost in Northern Ireland?

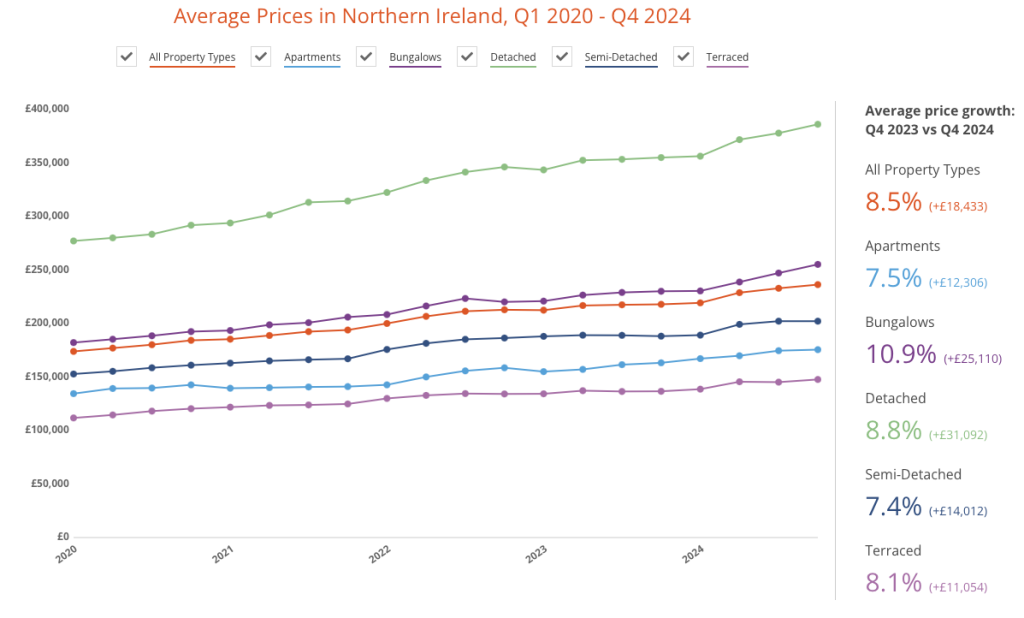

First of all, let’s look at probably the most important detail related to the purchase of a property, namely prices.

Statistics on property prices in Northern Ireland vary slightly depending on the source you use. According toPropertypal, in the fourth quarter of 2024, the average property price in Ireland was £236,395, which is £18,433 more than a year ago in the same period (8.5% difference). In the report for Q3 2024, Ulster University, on the other hand, reports a slightly lower figure of £219,110. While the differences between sources range up to 5%, there is a common denominator - property prices in Northern Ireland are much lower than the average figure for the UK as a whole, which you will read about in this article.

Over the last few years, property in Ireland has been gaining heavily in price - over the four years (from 2020 to the end of 2024), houses and flats have gained an average of 36% in value, while detached houses have become as much as 40% more expensive.

Source: Propertypal

Listings on Zoopla confirm that a 3-bedroom house can be found for less than £170,000! As usual, prices depend on a number of factors, such as location, property condition and amenities, but we can assume that, overall, homes in Ireland are noticeably cheaper than in England and Scotland.

Average property prices in Ireland by region

[

Region Average price Lisburn £284,707 Causeway Coast £265,130 Ards and North Down £293,846 Newry £250,546 Antrim and Newtownabbey £218,986 Mid Ulster £202,239 Mid and East Antrim £197,677 Belfast £219,440 Fermanagh £213,007 Armagh £203,807 Derry City £205,351 Buying a house in Northern Ireland - table of average property prices; Source: Propertypal

Tax on buying a property in Northern Ireland - SDLT

If you have read the articles on our blog, you probably know that when you buy a house in England, you have to pay tax on the transaction. This is known as Stamp Duty Land Tax (SDLT). For Northern Ireland, it’s all done in exactly the same way - you’ll find the rates and information on SDLT paperwork in this article.

We should also point out that in Northern Ireland you can take advantage of the First Time Buyer scheme. Due to lower property prices, you will most likely pay very low SDLT!

Changes to Stamp Duty Land Tax in 2025 - Northern Ireland

Unfortunately, from the first of April 2025, buying a home in Northern Ireland will become a tad less attractive, all thanks to the increase in Stamp Duty Land Tax that will take effect in April 2025. The reduction in the tax-free amount from £250,000 to £125,000 will inevitably mean that almost anyone deciding to buy a property in Ireland will pay at least a few hundred and up to £2,500 more.

Assistance schemes in Northern Ireland

As with the transaction tax (SDLT), Northern Ireland’s assistance schemes are very similar to those in England. Among the most important of these, are:

-

Right to Buy - this scheme allows you to receive a grant of £112,300 (£84,200 outside London). You will receive help if you have been renting a social housing property for a minimum of 5 years and the amount will depend on a number of factors;

-

First time buyer - by using this scheme, you will receive Stamp Duty Land Tax reduction relief;

-

Shared Ownership Scheme - this scheme allows you to buy a property jointly with the state - you buy a share and rent for the remainder. This is an excellent way to buy property for people who do not have a lot of savings.

Not sure if you qualify for any of the programmes? Get in touch with us! Together we’ll see if you can save some money on your purchase.

Is buying a house in Northern Ireland worthwhile?

Some of our clients wonder whether buying a house pays off more than renting. In the case of Ireland, we can answer almost unequivocally - yes! Although property prices there are clearly lower than in the rest of the UK, homes are rapidly increasing in value. In our view, prices are more likely to rise over the next few years, although we do not rule out the possibility that there may be periodic dips or slowdowns in the market.

In addition, property prices are always linked to rental costs. When giving an investment mortgage, the bank takes into account the expected rental income, so if rent becomes more expensive, so do houses.

The relationship between wages and property prices is also very attractive. The average annual salary in Northern Ireland is around 7% lower than in the UK as a whole, while property is around 20% cheaper (£236,000 instead of around £290,000). This means that living in Ireland will earn you an average house faster than you would in England. This trend is unfortunately waning - just two years ago, the difference was over 40%!

Buying a house to rent in Northern Ireland

Due to lower property prices, investing in a rental property in Ireland is more affordable. Although banks such as Barclays and HSBC continue to require a high deposit (minimum 25%), the lower purchase price means you need to prepare less cash to get a mortgage. Let’s also point out that you don’t have to live in Ireland to buy a rental property in Ireland - residence in any part of the UK also entitles you to benefit from the standard, rather than increased, rate of Stamp Duty Land Tax.

In addition, the rental property market in Northern Ireland is growing steadily. This means that yourBuy to Let mortgage could turn out to be a really good investment - you will be earning not only rent, but also the rising value of your house or flat. Thus, buying a house to let in Northern Ireland is akin to investing in a growing, successful dividend company on the stock market.

How long does it take to buy a house in Northern Ireland?

In favourable circumstances, buying a house in Northern Ireland takes between 2 and 3 months. During this time, we are able to go through all stages of the process, from choosing the right property to finding the solicitor needed for conveyancing and signing all the necessary documents.

If the situation is more complicated (e.g. there are problems with the legal status of the property, delayed moving out of the previous owners), buying a house can take up to six months. Usually, however, you manage to pick up the keys within 10-14 weeks of starting the whole process.

When you choose Extend Finance as your mortgage broker, you get the peace of mind that buying a home in Northern Ireland will be as quick, efficient and stress-free as possible. The icing on the cake, on the other hand, is cheap credit - you’ll only pay the bank as much as is absolutely necessary. We guarantee it!

Summary

We hope that our article has helped you in your decision to buy a home in Ireland. If it has, we would like to invite you to get in touch with us - your first consultation is free and doesn’t commit you to anything, and during the consultation, we will check your creditworthiness and together we will consider whether your dream of owning your own home is achievable now. We look forward to hearing from you!

FAQ

Frequently asked questions

How much does a house cost in Northern Ireland?

First of all, let’s look at probably the most important detail related to the purchase of a property, namely prices.

Tax on buying a property in Northern Ireland - SDLT?

If you have read the articles on our blog, you probably know that when you buy a house in England, you have to pay tax on the transaction.

Changes to Stamp Duty Land Tax in 2025 - Northern Ireland?

Unfortunately, from the first of April 2025, buying a home in Northern Ireland will become a tad less attractive, all thanks to the increase in Stamp Duty Land Tax that will take effect in April 2025.

Assistance schemes in Northern Ireland?

As with the transaction tax (SDLT), Northern Ireland’s assistance schemes are very similar to those in England.

Is buying a house in Northern Ireland worthwhile?

Some of our clients wonder whether buying a house pays off more than renting.