TL;DR

In short

- BMI (body mass index) is a relatively simple index showing the correlation of height to body weight.

- In the introduction to the blog, we mentioned that the body mass index affects life insurance and private medical insurance premiums.

- First of all, it should be noted that people who are both overweight and obese are at greater risk of many diseases.

- Definitely yes.

- As a rule, no.

BMI undeniably affects premiums for both life insurance and private medical policies. However, many of our clients do not realise how strong this impact is - in practice, people struggling with obesity suffer very serious consequences of their condition, including financially. Let’s find out exactly how body weight affects insurance premiums.

What is BMI?

BMI (body mass index) is a relatively simple index showing the correlation of height to body weight. The breakdown of BMI categories is as follows:

-

BMI below 18.5 - underweight

-

BMI between 18.5 and 24.9 - normal weight

-

BMI between 25 and 29.9 - overweight

-

BMI between 30 and 34.9 - obese

-

**BMI over 35 **- extreme obesity

Of course, the body mass index is subject to a large degree of error and this view is relatively common among doctors. For example, it does not distinguish between muscle mass and body fat, but it is basically the only way to quickly estimate whether or not an insurance company’s client is overweight or obese.

Our practice shows that a significant proportion of people taking out life insurance in the UK tend to underestimate their weight and overestimate their height. This view is also confirmed by Zurich, one of the largest companies in our industry.

Which insurance prices are affected by BMI?

In the introduction to the blog, we mentioned that the body mass index affects life insurance and private medical insurance premiums. These are the most common examples, but certainly not the only ones. In our experience, body mass often affects the cost of critical illness insurance and, less commonly, accident insurance.

In general, the insurance premium for an overweight or obese person will be higher if the benefit payment is conditional on a sudden deterioration in health or loss of life.

BMI, on the other hand, does not affect your property insurance premiums - your auto-insurance, motor liability insurance, home or contents policy or professional indemnity insurance will not be more expensive if you are struggling with overweight or obesity.

Why does BMI affect insurance premiums?

First of all, it should be noted that people who are both overweight and obese are at greater risk of many diseases. The cardiovascular system as well as the musculoskeletal system are under greater strain, and the risk of cancer is also increased. This in turn leads to a greater likelihood of premature death as well as hospitalisation.

From an insurance company perspective, people with a higher body mass index are riskier customers. Overweight people (BMI 27) have a 20-30% higher risk of premature death compared to those with a body mass index of 25. The client’s general health is also an additional factor affecting premiums - obesity-related co-morbidities such as diabetes, hypertension and elevated cholesterol levels can also translate into receiving worse terms and conditions. This is how the regulations of companies such as Guardian, for example, are structured.

What about underweight?

This side of the coin is discussed far less often, but underweight people can also pay more for their insurance. This will be especially apparent to elderly clients, as they are at particular risk of fractures, the occurrence of osteoporosis and falls. It may even be the case that someone who is slightly overweight will pay lower premiums than someone who struggles with being clearly underweight.

It is inevitable that in order to make it profitable to sell a policy to a customer with too low or too high a BMI, premiums must be higher - after all, the insurance company does not want to be at a loss. This would be illogical.

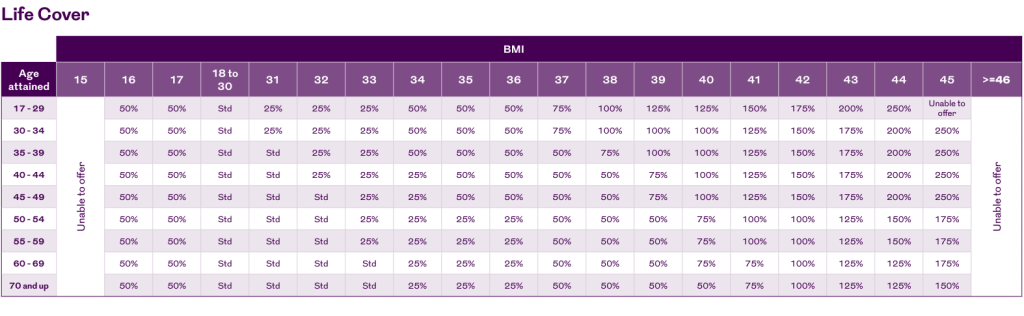

Does age have any impact on BMI in insurance terms?

Definitely yes. For some insurance companies, the extent to which BMI affects premiums depends on the age of the person applying to purchase the policy. An example is the Royal London offering:

From the table above, the relationship is quite simple - being overweight and obese at any age translates into higher insurance premiums, but the younger you are, the higher the surcharges will be. In extreme cases, a policy for a very young person will be up to 100% more expensive than one for a person of retirement age.

Does Body Mass Index always translate into insurance costs?

As a rule, no. Even if you are slightly overweight, the premiums on your life insurance policy can remain at the standard level. The decision is always up to the insurer and depends on the internal policy of your chosen company.

If you are over 50 years of age, a BMI between 25 and 30 may be considered normal by your insurer. This is due to the aforementioned inaccuracy of BMI, which does not take into account the changes in body composition that occur with age in people.

How much higher a premium will I pay if I have a high BMI?

The data we have shows that in the vast majority of cases, a BMI above the 18.5-25.0 range translates into an increase in premiums of no less than 25% and no more than 250%.

In the case of critical illness insurance, this relationship is perfectly illustrated in the table below:

Age BMI Amount of the premium 17 - 30 18,5 - 25,0 Standard 17 - 30 25,1 - 30,0 From 125% to 150% 17 - 30 30,1 - 35,0 From 150% to 175% 17 - 30 35,1 - 40 From 175% to 250% 17 - 30 40 and more The contract will not be concluded 31 - 49 18,5 - 25,0 Standard 31 - 49 25,1 - 30,0 From 100% to 125% 31 - 49 30,1 - 35,0 From 125% to 175% 31 - 49 35,1- 41,0 From 175% to 250% 31 - 49 41 and more The contract will not be concluded 50 and more 18,5 - 30,0 Standard 50 and more 30,1 - 35,0 From 100% to 125% 50 and more 35,1 - 40 From 125% to 200% 50 and more 41 and more The contract will not be concluded Sources: Criticalillness.org.uk; own calculations

Two interesting relationships emerge from the table above. Firstly, the younger you are, the more you will feel the financial consequences of a higher BMI. This is, of course, due to the longer period of time your body will be under severe strain.

Secondly, even being slightly overweight can clearly increase premiums. Given the long-term nature of insurance contracts and the average monthly cost of £25.16, even a 25% uplift translates into an extra £754.8 over a decade.

FAQ

Frequently asked questions

What is BMI?

BMI (body mass index) is a relatively simple index showing the correlation of height to body weight.

Which insurance prices are affected by BMI?

In the introduction to the blog, we mentioned that the body mass index affects life insurance and private medical insurance premiums.

Why does BMI affect insurance premiums?

First of all, it should be noted that people who are both overweight and obese are at greater risk of many diseases.

Does age have any impact on BMI in insurance terms?

Definitely yes.

Does Body Mass Index always translate into insurance costs?

As a rule, no.