TL;DR

In short

- In early February, the Bank of England cut interest rates by 25 basis points , setting the benchmark interest rate (bank rate) at 4.

- As interest rates gradually fall, so do monthly instalments over the Initial period of the mortgage.

- With the impending changes to the Stamp Duty Land Tax, property prices in the UK have reached record levels, with the average approaching £300,000 .

- It is easy to guess that the rise in UK property prices has also made renting houses and flats more expensive.

- When considering a home in the UK as an investment for the future, it is worth being aware of the demographic outlook.

Buying a house will probably be the biggest expense of your life. It involves a lot of paperwork and is often also very stressful. One of the most important steps on the path to your own property is taking out a mortgage to finance the purchase. In this article, we’ll outline the realities of the UK property market in 2025, look at typical mortgage terms and, most importantly, help you answer the question of whether it’s worth buying a home in the UK in 2025.

Interest rates

In early February, the Bank of England cut interest rates by 25 basis points, setting the benchmark interest rate (bank rate) at 4.5%. All indications are that this decision is a continuation of the November 2024 action - the interest rate cuts are designed to reheat the economy after inflation has fallen to acceptable levels.

Although we are currently experiencing very high interest rates, as they reached their highest level since 2008 in August 2023, such a situation will probably not last for too long. We expect the Bank of England to cut interbank lending rates again in the near future, although it is difficult to expect money to be as cheap as it was back in 2020 and 2021, when the base rate was just 0.1%.

When buying a home in the UK, you need to think long-term - you’ll be paying back your loan over 20, 25 or even 30 years. While no one can predict what will happen decades in the future, the nearer future is already much easier to describe - according to theBBC, financial markets are predicting up to three more interest rate cuts in 2025, but this is only speculation. Bank of England Governor Andrew Bailey has limited himself to saying that he will consider further interest rate cuts, but will approach the subject gradually and cautiously.

So what can be inferred? Current mortgage rates in the UK are not excessively low, but the days of record high installments are behind us. Moreover, in our opinion, gradual reductions in interest rates are possible, although this must not be taken for granted.

How are mortgage instalments changing in the UK?

As interest rates gradually fall, so do monthly instalments over the Initial period of the mortgage. For Tracker mortgages, whose interest rates react very quickly to changes in base rates, instalments are decreasing year on year - according toHSBC bank rates, in January 2024 the mortgage instalment during the promotional period was as much as 7.5% higher, compared to today. On a £300,000 mortgage with an LTV ratio of 90%, the monthly mortgage instalment in January 2024 would be £1,958.66, compared to £1,822.61 today, which translates to as much as £1,632 a year less overall.

The table below shows the indicative values of monthly instalments for fixed-rate mortgages with a 24-month term in January between 2023 and 2025. The interest rate depends on a number of factors, such as your own contribution, your creditworthiness and the bank’s policy. It is also worth bearing in mind that each person may receive a bespoke offer, so the figures shown are for illustrative purposes and are taken from HSBC’s historical bank data, which is published on its website.

Date Mortgage amount Deposit Interest rate (first 2 years) Monthly instalment January 2023 £300,000 10% 5,24% £1,795.97 January 2024 £300,000 10% 4,99% £1,752.02 January 2025 £300,000 10% 5,09% £1,769.54

Similar values are shown by our mortgage comparison engine. Examples of monthly instalments on these terms include:

-

£1,734.60 in Leeds Building Society

-

£1,746.79 in Santander Bank

-

£1,750.28 in The co-operative Bank

To illustrate the importance of a large down-payment, below is a table with examples of instalments, with the LTV reduced to 75%.

Date Mortgage amount Deposit Interest rate (first 2 years) Monthly instalment January 2023 £300,000 25% 4,7% £,1701.73 January 2024 £300,000 25% 4,69% £,1700.01 January 2025 £300,000 25% 4,44% £,1657.29

It is worth noting that back in January 2023, interest rates set by the Bank of England were just 3.5% and were only just starting to rise. Their first reduction was introduced in August 2024 and since then, interest rates have been falling - and with them the monthly instalments on tracker mortgages.

Property prices

With the impending changes to the Stamp Duty Land Tax, property prices in the UK have reached record levels, with the average approaching £300,000.

In our article on house prices, you can read about the latest UK House Price Index report, which looks at the market situation in November 2024 - in that month, the average property price was £289,707. That’s around £9,000 more than the year before!

Such a surge is due to increased demand for housing as a consequence of the impending increase in Stamp Duty Land Tax rates. January this year saw a 0.7% increase in property sales compared to the previous month, and forecasts indicate that by 2025, property prices are expected to rise by 2.5% and the number of transactions could increase by as much as 5%. These figures do not look surprising, but even a small percentage increase means billions of pounds impacting the property market.

Rising property prices may discourage those who are just preparing to buy a property, but on the other hand, a timely enough purchase can prove to be a good investment. Houses and flats in the UK have mostly been getting more expensive over the last few years and we expect that interest rate cuts will only accelerate this process.

Those who are determined to move should definitely consider taking action as soon as possible, in a way that avoids paying more SDLT tax. There is little time left to implement the changes, as they come into effect on 1 April, alongside the new tax year. The only way that UK home buyers will be able to pay SDLT tax at the current rates is if they plan for a completion date before 31 March 2025. In the table below, we outline the change in the Stamp Duty Land Tax thresholds.

Part of the value of the property Rate before change Rate after change Up to £250,000 0% Up to £125,000 0% £125,001 to £250,000 0% 2% £250,001 to £925,000 5% 5% £925,001 to £1,500,000 10% 10% Above £1,500,000 12% 12% You can read more about the changes to SDLT in our article ‘Stamp Duty Land Tax on property purchases in 2025. What has changed?’

How have rents changed?

It is easy to guess that the rise in UK property prices has also made renting houses and flats more expensive. The average rentin January 2025 was £1,327 per month, which is £110 more than a year ago. On its own, this information is unimpressive until you contrast it with other statistics.

Over the last three years, rents have increased by around 37% from £969 to £1,327. This was, of course, due to rising interest rates - landlords had to compensate for risingbuy-to-let mortgageinstalments on their properties. The recent reduction in borrowing costs will probably mitigate this, but we doubt that rents will fall.

It is also worth comparing the value of an annuity to a mortgage instalment - using the aforementioned interest rate of 5.39%, we can calculate that on a 25-year mortgage , an instalment of £1,327 allows for a mortgage repayment of £218,500. This is obviously less than the value of the average property in the UK, which has exceeded £280,000 for a long time. In doing so, economists point out that renting homes is becoming increasingly unaffordable for people - prices are rising faster than wages.

Looked at this way, rising rents should motivate you to buy a property as soon as possible. The mortgage instalment will be an additional burden for you, but it will build your wealth.

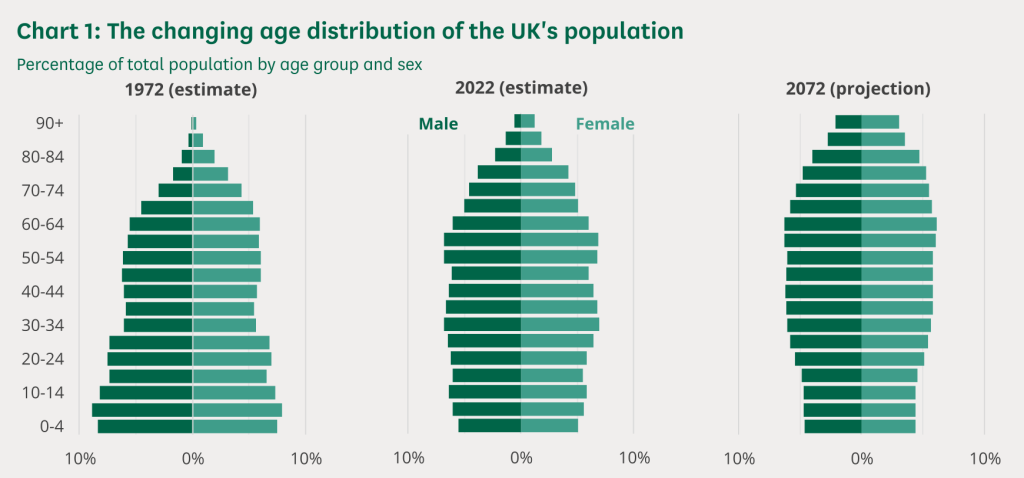

How are demographics affecting the UK property market?

When considering a home in the UK as an investment for the future, it is worth being aware of the demographic outlook. First and foremost,** the number of people living in the UK is growing year on year - in 2023, over 600,000 people will have arrived.**

The large proportion of young people in the population means that a home in the UK can be a good investment. Graphic source: House of Commons

Everyone needs somewhere to live, so unless the government takes action to curb property prices, your UK home is likely to appreciate in value over time. An annual population growth rate of 1% doesn’t sound impressive, but this phenomenon also needs to be considered in the long term - in twenty years’ time, that’s around 12 million people, or one and a half times the population of London!

Is it worth buying a house in the UK in 2025?

Let’s face it - owning your own home in the UK is no longer as viable an investment as it was just a few years ago. Mortgage interest rates are relatively high, purchase tax is about to rise, due to the relatively high cost of living, your affordabilityis probably low. However, pessimism is not warranted - every year of renting leaves you leaving thousands of pounds more with your landlord instead of building up your wealth.

So would we personally choose to buy a house in the UK? By all means! Although there is no denying that there are periodic price drops in the property market, with gradual repayment, a mortgage becomes an investment in a secure future. The sooner you decide to buy your own property, the sooner you can gain financial freedom, and in 20 years’ time, the difference of even a few thousand pounds in the price of a house will no longer have any real significance.

FAQ

Frequently asked questions

Interest rates?

In early February, the Bank of England cut interest rates by 25 basis points , setting the benchmark interest rate (bank rate) at 4.

How are mortgage instalments changing in the UK?

As interest rates gradually fall, so do monthly instalments over the Initial period of the mortgage.

Property prices?

With the impending changes to the Stamp Duty Land Tax, property prices in the UK have reached record levels, with the average approaching £300,000 .

How have rents changed?

It is easy to guess that the rise in UK property prices has also made renting houses and flats more expensive.

How are demographics affecting the UK property market?

When considering a home in the UK as an investment for the future, it is worth being aware of the demographic outlook.