TL;DR

In short

- Whether a bank agrees to grant a mortgage for a particular property should not be the sole indicator of whether the purchase is a sound investment .

- Crime rate One of the most important factors that significantly reduces the appeal of a particular location is a high crime rate .

- There are several key factors you should consider before buying a house in the UK.

A property purchased to provide a home for you and your family should be a place where everyone feels safe, children have access to a high standard of education, and the location itself genuinely improves your quality of life. Equally important is long-term financial security – buying a home that is depreciating in value can expose the owner to the risk of negative equity, i.e. a situation where the property’s value falls below the amount of the mortgage.

To help you make an informed decision, we have prepared an article discussing the key factors that could make buying a house in a particular location a poor investment.

Does a bank’s approval of a mortgage mean the purchase is a sound investment?

Whether a bank agrees to grant a mortgage for a particular property should not be the sole indicator of whether the purchase is a sound investment. Of course, banks sometimes reject a mortgage application due to the property’s characteristics or its location, but this only happens in extreme cases where analysts consider that granting such a mortgage could expose the bank to a real financial loss.

In many cases, the bank will agree to grant a mortgage even though the property in question may cause you many problems or expose you to financial difficulties. Remember that what matters to lenders is that you will be able to repay the mortgage – you must take care of your family’s safety and your quality of life yourself. Provided your financial situation is not complicated, you are not applying for a very large sum, and you are not attempting to buy a house with structural defects, the bank will not scrutinise the property you are buying too closely – it must be fit for habitation, fairly valued, and not require immediate renovation. However, no one will stop you from buying a house in a noisy or poorly connected neighbourhood, and the same applies to flats in areas with a high crime rate.

Therefore, before you buy a property, you should carry out proper research into the location of your potential home.

What risk factors should you consider when buying a house in the UK?

Crime rate

One of the most important factors that significantly reduces the appeal of a particular location is a high crime rate. This problem is affecting more and more towns and cities across the UK, making residents feel increasingly unsafe. When considering your family’s safety in your chosen neighbourhood and a long-term financial commitment, it is definitely worth analysing the crime rate in the area. Bear in mind that the number of thefts can even affect the cost of your car insurance premiums.

There are several sources from which you can obtain information. One of them is official government websites, such as:

-

UK Police Crime Map – a website dedicated to statistics on various crimes occurring in specific areas. Using the search function, you can check a specific neighbourhood in England, Northern Ireland and Wales;

-

in the case of Scotland, finding information will be slightly more difficult, as there is no interface as straightforward as that of the rest of the UK, but the information is still available on the Scottish Police website. Alternatively, you can find various summaries and interpretations of the data online, e.g. datamap-scotland;

-

Office for National Statistics (ONS) – the website of the UK’s largest independent statistical office.

In addition to official statistics, information on crime in a given region can also be found on online forums such as Reddit or Mumsnet, where users often share their experiences of everyday life in specific towns and cities. There is also nothing to stop you from asking members of the local community for their opinions yourself.

However, you should bear in mind that information posted on forums is not always entirely reliable. For this reason, it is best to treat it merely as supplementary information, and to base key decisions primarily on official and verified data.

The most dangerous places to live in the UK

When you look at crime statistics, you’ll very quickly be able to draw the correct conclusion – large cities are the most dangerous. However, you must remember that choosing where to live is a very local decision, not one that applies to the whole city, so it’s better to check each neighbourhood in detail.

For example, in London, the most dangerous neighbourhood is Westminster, which stands out with a crime rate of a staggering 366.9 offences per 1,000 people. Second in the ranking is Camden, whose crime rate is around half that, at 186.4 per 1,000 people. Islington, Nottingham, Westminster and Bristol also face high levels of crime.

Sources: eufy.com, mirror.co.uk

When we look at the statistics, the variation can be quite significant – for example, in Bradford, statistically the most dangerous city in the UK, you could easily consider moving to Wharfedale, where the crime rate is just 41.4 offences per 1,000 people.

When choosing the location of your new home, you should take the time to analyse crime levels in your chosen areas in detail. This will enable you to provide your family with a safe life within a peaceful community, even in cities with a bad reputation. However, it is worth weighing this up against other criteria – such as the local job market, access to schools and the number of shops.

Standard of education

Assessing the standard of educational institutions in a given location is crucial for two reasons. Firstly, this obviously has a direct impact on your children’s educational journey. If schools offer a low standard of teaching, they may fail to provide suitable conditions for your children’s development and expose them to difficulties arising from inadequate educational support. Even if you manage to find a suitable school for your child further away from home, long daily commutes can reduce your family’s quality of life, making such a solution completely impractical.

Furthermore, the standard of local schools is a factor that significantly influences the property market in a given area. Bear in mind that every parent will want to ensure their children receive a good education, so demand for residential property in such areas may be much lower, as families will tend to avoid them. As a result, when you decide to sell the house, it may be much more difficult.

Although there is a chance that the situation will improve over the years, buying a house in an area with poor educational facilities carries a financial risk – if the quality of schools and the general standard of the neighbourhood do not improve, the property’s value may rise more slowly than in other areas, and in extreme cases may even fall. Therefore, even if you do not have or are not planning to have children, buying a house in such a location is still risky.

To assess the standard of educational establishments in a particular area, it is best to consult the reports published by Ofsted (the Office for Standards in Education, Children’s Services and Skills), the government body responsible for monitoring and evaluating the quality of education and care for children and young people.

Economic and development prospects

Around 60% of our clients choose to buy a house or flat in a different neighbourhood from the one where they have previously rented. Interestingly, there is also a large group of people who decide to move to a different town, often within the same urban area. When choosing a place where you plan to spend hundreds of thousands of pounds on a house, it is worth thinking more broadly than just about your current job.

In the UK, there are many towns and cities that have been shrinking for years due to internal migration – such places may be attractive because of low property prices, but in the long run they may not provide suitable living conditions for your family.

There are several good examples of such towns and cities:

-

**Blackpool **– a town on the west coast, about 50 miles north of Liverpool. For decades, the town was a popular holiday resort, which largely provided it with income and jobs. Following the decline in domestic mass tourism, many resorts went out of business and their employees had to retrain. As a result of these changes, the town began to struggle with high unemployment and social problems in certain neighbourhoods;

-

**Middlesbrough **– a town on the east coast, about 70 miles north of Leeds. Middlesbrough developed as a major centre of heavy industry, which formed the backbone of the local economy. In the second half of the 20th century, as heavy industry across Europe began to decline and factories started closing, the town began to lose stable jobs. Despite several attempts at regeneration, Middlesbrough continues to face economic and social challenges;

-

**Burnley **– a town situated halfway between Preston and Bradford – like Middlesbrough, Burnley has suffered the most from the economic changes of the 20th century. Once famous for its textile industry, it now faces many problems, such as unemployment and a high crime rate.

Of course, we’re not saying that you definitely shouldn’t buy a house in these towns, let alone move away from them. These examples simply highlight places whose heyday is now behind them, and living there could be risky both financially and in terms of overall development.

It is therefore a good idea to take a look at unemployment statistics or local council reports and analyse the situation before making a final decision.

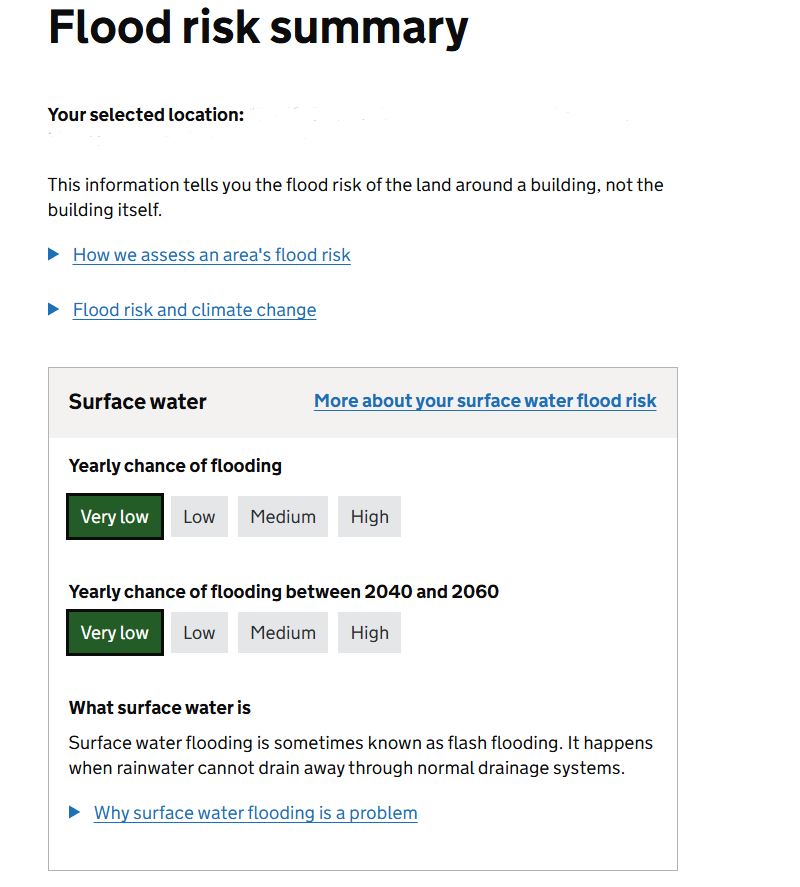

Flood-prone areas

As many as 20% of all properties in the UK are at risk of flooding. Before you buy a house at a particular address, be sure to check its flood risk classification. To do this, use the tool on the government website. If it shows a ‘high’ risk, you should think twice about your decision. Even if a bank were to grant a mortgage for such a property, you would be exposing yourself and your family to significant problems associated with flooding in the event of a flood.

Summary

There are several key factors you should consider before buying a house in the UK. Bear in mind that a low property price does not necessarily mean a good deal; it may be a sign of an unsafe neighbourhood, a risk of flooding, or a low standard of local services.

FAQ

Frequently asked questions

Does a bank’s approval of a mortgage mean the purchase is a sound investment?

Whether a bank agrees to grant a mortgage for a particular property should not be the sole indicator of whether the purchase is a sound investment .

What risk factors should you consider when buying a house in the UK?

Crime rate One of the most important factors that significantly reduces the appeal of a particular location is a high crime rate .

Summary?

There are several key factors you should consider before buying a house in the UK.

What should I know?

The key details are explained in the article above. If you are unsure, it is worth speaking with an adviser before making a decision.

What should I know?

The key details are explained in the article above. If you are unsure, it is worth speaking with an adviser before making a decision.