TL;DR

In short

- Many people are unable to give a concise answer to this question, when in fact it is quite simple.

- As you might expect, forecasting interest rates is easier the shorter the time horizon.

- When we talk about a time horizon of a decade, forecasting becomes very difficult.

- Thirty years is a very long time – during that period, absolutely anything can happen, including achange of job, the arrival of a new baby, or even the death of the borrower.

- Six months ago, we prepared a comprehensive article on this topic, so for a more detailed answer to this question, it is worth visiting that site.

As a legally operating credit broker in the UK, we must inform our customers about the risk of interest rate increases and, consequently, increases in their mortgage instalments. Although this seems obvious, few people consider the actual likelihood of such an event occurring. For this reason, in today’s post, we will examine the prospects for borrowers over a period of several years and several decades.

For the sake of clarity, let us add that anything that is not described as a quotation or supported by specific statistics should be interpreted as the personal opinion of the author of this article. Like everyone else, we may simply be wrong. However, we strive to base our beliefs on scientific views and economic data.

Why do mortgage interest rates change at all?

Many people are unable to give a concise answer to this question, when in fact it is quite simple. Interest rates on mortgages are derived from the Bank of England’s reference rate, which is a tool used to control lending opportunities in the economy. When interest rates are high, borrowing becomes more difficult. At that point, the economy slows down, inflation falls, and the pound gains value against other currencies. However, people can afford less than before the rate hike. When rates are lowered and borrowing becomes easier, inflation can spiral out of control, which also causes a wave of price increases.

Although we could write a book on the role of interest rates, let us limit ourselves for now to saying that low interest rates on loans will drive the economy and raise inflation, while high interest rates will have the opposite effect. For this reason, our forecasts will be influenced primarily by economists’ forecasts.

Will mortgage interest rates rise over the next two years?

As you might expect, forecasting interest rates is easier the shorter the time horizon. Of course, a lot of unexpected events can happen in two years, but it can be assumed that the risk of them occurring is relatively low.

In our opinion, interest rates on mortgages in the UK will slowly decline or remain unchanged in the near future. Fairly high inflation (3.8% per annum), a relatively low risk of an economic slowdown in the near future and the widespread problem of buying a first property mean that the BoE will probably want to gently lower the base rate, although it cannot afford to make any sudden moves. Economists estimate the probability of interest rate cuts this year at around 20%, although it is worth noting that forecasts are subject to frequent changes.

However, the current situation is definitely not bad – stable interest rates on mortgages mean that the risk of entering into negative equity is much lower, and instalment amounts will be predictable. This, in turn, makes it easier to plan expenses.

What will happen to interest rates in the next 5-10 years?

When we talk about a time horizon of a decade, forecasting becomes very difficult. On the one hand, we will almost certainly experience a crisis and another market recovery during this period. On the other hand, however, 10 years is still not enough to be able to talk about long-term trends that can be observed over a period of twenty, forty or fifty years.

It is safe to assume that after interest rates on mortgages are likely to fall over the next 2-3 years, this trend will reverse . It is difficult to give specific percentages, but in our opinion, over the next decade, the Bank Rate will probably approach both around 1% and perhaps 5%, as was the case a year ago.

How will the interest rate on my mortgage change over 30 years?

Thirty years is a very long time – during that period, absolutely anything can happen, including achange of job, the arrival of a new baby, or even the death of the borrower. Although your personal life is likely to undergo enormous changes, in economic terms, the future does not have to be so turbulent.

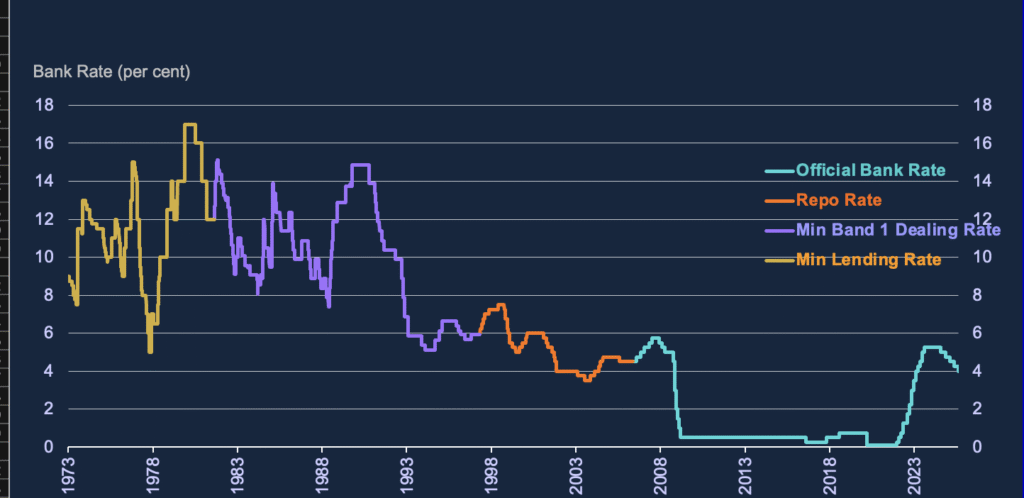

Source: Bank of England

Economics, like any science, is evolving. The Bank of England and other central banks are using knowledge more and more effectively, making inflation control easier and more effective than it was 20 or 30 years ago. The optimisation of monetary policy translates into lower interest rates on mortgages and less radical changes in interest rates. This is clearly illustrated by the interest rate charts for 1978-1993 and 2009-2020.

Although absolutely anything could happen in the future, it is highly likely that interest rates on mortgages and credits will gradually decrease in the long term. It cannot be ruled out that in 20 years’ time there will no longer be such drastic changes as those seen in 2022-2024.

So what should I do? Is 2025 a good time to take out a mortgage?

Six months ago, we prepared a comprehensive article on this topic, so for a more detailed answer to this question, it is worth visiting that site. For the purposes of this post, let us just note that both the current interest rates on mortgages and property prices in relation to earnings make 2025 a fairly good time to move. Of course, 4-5 years ago it was possible to buy property more cheaply, but 2020 and 2021 were a special time in history – the pandemic caused enormous turmoil in the market.

We are also convinced that in 10-20 years’ time, today’s house and flat prices will evoke nostalgia in us. In the long term, real estate gains in value, and although temporary fluctuations are natural, there has never been a situation where, after a decade or two, the average house was worth less than at the time of purchase.

FAQ

Frequently asked questions

Why do mortgage interest rates change at all?

Many people are unable to give a concise answer to this question, when in fact it is quite simple.

Will mortgage interest rates rise over the next two years?

As you might expect, forecasting interest rates is easier the shorter the time horizon.

What will happen to interest rates in the next 5-10 years?

When we talk about a time horizon of a decade, forecasting becomes very difficult.

How will the interest rate on my mortgage change over 30 years?

Thirty years is a very long time – during that period, absolutely anything can happen, including achange of job, the arrival of a new baby, or even the death of the borrower.

So what should I do? Is 2025 a good time to take out a mortgage?

Six months ago, we prepared a comprehensive article on this topic, so for a more detailed answer to this question, it is worth visiting that site.