TL;DR

In short

- Debt to Income Ratio is the ratio of your monthly liabilities to your income.

- Let us list the most important ones: Mortgages; Buy to let investment mortgages; Loans; Lease and hire purchase instalments (leases); Funds borrowed on credit cards.

- The Debt to income ratio is an important factor from the perspective of the creditworthiness assessment made by bank underwriters.

- According to most lenders, the maximum DTI is 60% and it is the factor that influences the amount you can borrow affordability, which is usually calculated as 4.

- Your Debt to Income ratio does not directly affect your credit score.

Banks look at a great many factors when assessing affordability. One of them is the Debt-to-Income ratio, or in other words the debt-to-income ratio. Its value signals your ability to repay and, in a sense, determines the lender’s level of risk.

What is the debt-to-income ratio?

Debt-to-Income Ratio is the ratio of your monthly liabilities to your income. So if your DTI is 20% and you earn £5,000 a month, the total of your instalments on loans, advances and leases will be £1,000.

DTI = ((total of your liabilities) / (your gross income)) * 100%

What commitments affect the DTI?

Let us list the most important ones:

-

Mortgages;

-

Loans;

-

Lease and hire purchase instalments (leases);

-

Funds borrowed on credit cards.

By convention, fixed liabilities that are not loans do not count towards the Debt-to-Income ratio - so we do not include private school tuition fees, subscriptions, subscriptions, etc. A credit card limit also does not increase the DTI level - only real liabilities that need to be repaid count.

Why is the Debt-to-Income ratio important?

The Debt-to-income ratio is an important factor from the perspective of the creditworthiness assessment made by bank underwriters. The DTI ratio is also important in terms of credit risk.

Debt-to-Income and affordability

According to most lenders, the maximum DTI is 60% and it is the factor that influences the amount you can borrow - affordability, which is usually calculated as 4.5 times your annual income, is simply derived from DTI.

If 20% of your income is taken up by loan repayments, credit card repayments and other obligations, you are left with around 40% of your salary to repay the mortgage. It does not matter what proportion of your earnings you allocate to savings, for example - the DTI is set at a relatively low level because, if interest rates rise, your mortgage instalments could increase dramatically, potentially even exceeding your income. History unfortunately knows of such cases.

It is reasonable to assume that those with above-average earnings will be able to find banks that accept a higher DTI - for example, 70%. After all, no one should be surprised that someone with annual earnings of £200,000 will need a smaller proportion of their income to cover basic living costs compared to someone earning £35,000.** Earning very little, you may be condemned to a lower DTI** - for example, 40%.

Debt-to-income and credit risk

Your Debt-to-Income ratio does not directly affect your credit score. However, it is a very important indicator from a risk assessment perspective - if your DTI changes frequently, a credit analyst may infer that your financial situation is not very stable. Similarly, by keeping your DTI low and stable, you give evidence that you are managing your money well and not taking on all possible liabilities.

Logic would dictate that a** low Debt-to-Income Ratio is evidence of prudent and responsible money management**. People with low borrowing needs tend to have their finances under control.

What amount of debt-to-income ratio is considered good?

It is very difficult to give a specific DTI figure that can be considered adequate. In theory, it is of course 0%, but it is hard to expect a UK adult to have no liabilities. The average household has loan commitments of around £17,000, while almost 30% of families are paying off their mortgage, with an average balance of £193,000. It can therefore be considered that on average we are talking about around £75,000 per family.

In our opinion, a debt-to-income ratio of less than 20% is a very good result. If your liabilities take up less than 20% of your gross monthly income, basically no bank will refuse to lend to you. This is also the level at which you will be able to withstand a rise in interest rates in peace. Even if your total instalments were to double, you will still be able to afford them.

Debt-to-income of between 20% and 40% is also a good result. There should be no problems with getting a mortgage - this is the DTI that a large proportion of our customers have. If you have an adequate supply of savings and do not make decisions impulsively, you are unlikely to have to fear financial problems or a rejected credit application.

Debt-to-income of 40% to 60% suggests that the situation needs to be worked on. Exceeding 50% DTI means that the range of available lenders narrows noticeably and the terms of the mortgages on offer are not very good. In our view, you should do everything you can to get your DTI down to around 40% before applying for a mortgage. As well as having access to better deals, you will also gain a much higher level of mental comfort.

Debt-to-income of between 60% and 80% is an alarming score that severely limits the availability of credit offers. You will find it extremely difficult to get a mortgage with a low deposit, and analysts will also be more meticulous when it comes to assessing your credit score. A DTI above 60% is already basically financial instability.

Debt-to-income above 80% makes obtaining a mortgage a challenge. Banks are wary of working with people with high levels of debt, as even small changes in interest rates can lead to their insolvency and delayed instalments.

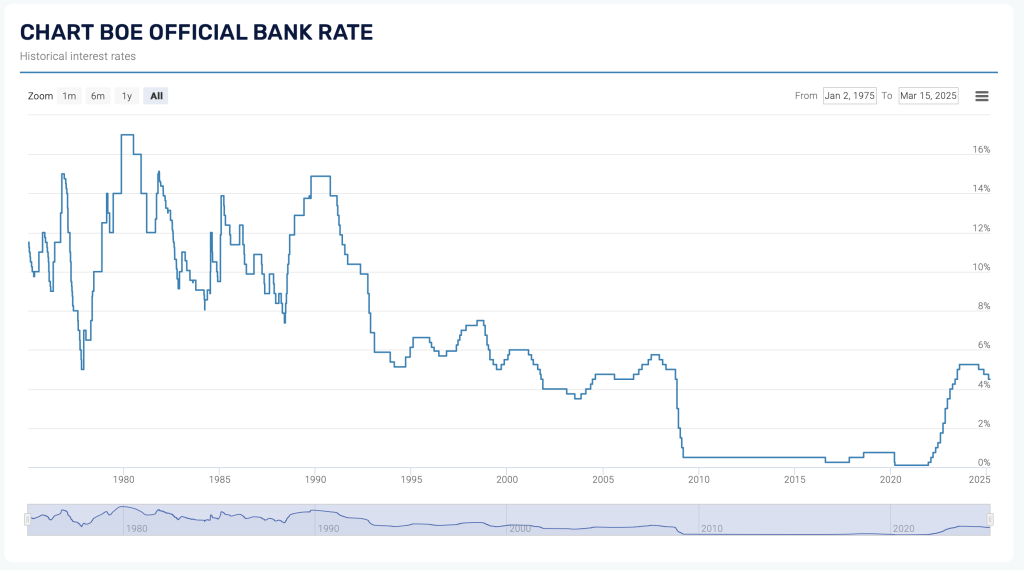

How does debt-to-income vary with the level of interest rates?

Current interest rates in the UK are relatively high, at 4.5% in March 2025. This is very high compared to 2009-2022, but when looking at a longer slice of history, it is important to be aware that in the 1980s lending rates could exceed 20%. These times are unlikely to return, as the nature of the global economy has clearly changed. Therefore, when taking out a mortgage, you must expect the risk of an increase in interest rates.

Source: global-rates.com

In fact, one does not need to go back to the 1980s to see how painful changes in Bank of England policy can be. To illustrate this, let us use an example.

In January 2021, Anna and Maximilian took out a £190,000 mortgage with a £10,000 or 5% down-payment. Initially, the interest rate was 2.6% and was frozen for 2 years. The repayment of the entire commitment was spread over 25 years. Anna and Maximilian were then paying instalments of £861.97 per month. Thanks to the low interest rate, they managed to give back £11,081, so their mortgage balance was £178,919.

When their mortgage agreement came to an end two years later, the situation was already very different - interest rates had risen, making the available offers much less favourable. Anna and Maximilian decided toremortgage and, despite a much lower LTV, the interest rate was already 4.2%. The instalment was already £1,012.06. Between January 2023 and January 2025, they managed to reduce the mortgage balance by just £9,643, so it had fallen to £169,276.

In January 2025, Anna and Maximilian remortgaged again. They did not want to extend the repayment period, so they took out a 21-year loan at an interest rate of 5.7%. The instalment increased again - this time to £1,153.53. In January 2027, their mortgage balance will be £160,414, so they will only manage to repay £8862 over two years.

Between January 2021 and January 2027, the protagonists of the example would repay £29,586 of capital. In a hypothetical scenario where interest rates would have remained at the same level as in January 2021, they would have been able to repay in six years…. £35,047.

Let’s also compare the instalments. Assuming fixed and low interest rates, Maximilian and Anna would give £62,061.84 to the bank. In practice, however, it will be** £72,661.44.** The difference is over £10,000! It is worth noting that with each increase in the monthly instalment, the Debt-to-Income ratio of Maximilian and Anna increases.

If you are curious about how your mortgage instalments will develop in the future, it is worth using the mortgage calculator created by Moneyhelper. We have also used it.

You can read more about the risks associated with interest rate changes in the article entitled ‘How do changes in interest rates affect mortgage repayments?’.

Mortgage stress test

The above example was not intended to scare you - it is simply about realising that it is not worth getting used to your current mortgage rate.

Until recently, lenders had to perform a so-called mortgage stress test. This involves checking whether the mortgage applicant will be able to pay the instalments if they increase. However, the FCA’s official guidance did not include information on the maximum Debt-to-Income ratio after such an increase, nor how accurate the test should be. In many institutions, a 3% interest rate increase was used as a criterion.

The stress test has now been withdrawn. The official reason for this is the desire to increase the availability of mortgages and the low likelihood of interest rates rising in the near future.

Ways to reduce the debt-to-income ratio

At the outset, let us point out - the ways in which debts are managed should depend on several factors, such as:

-

Your age - at 50 you can’t afford to extend the term of a commitment such as a mortgage much. What’s different if you’re 30 and have 3 decades of working life ahead of you;

-

Your income and the potential to increase it - if your job allows you to get a promotion or take overtime, you are in a much better position than someone who is no longer able to earn more in their current job;

-

Debt structure - you’ll experience a much bigger change if you’re paying off loans with high interest rates, because by getting rid of them, you’ll reduce your repayment expenses a lot more;

-

The current market situation - current interest rates have a big impact on your debt management strategy;

-

Your expenses in the future - paying off debts at the expense of savings is not always advisable.

Extension of the repayment period of loans and credits

Changing the repayment schedule of a loan or credit is a way to basically guarantee a reduction in the Debt-to-Income Ratio - you will end up having more time to pay back all the capital, so the instalments will be lower. Unfortunately, this translates into a higher total cost of the loan, as interest will take longer to accrue.

Extending your repayment period is sensible if you are relatively young. You need to remember that about 10 years before you plan to retire, you should focus on putting money aside for it. Mortgages, leases and loans can make this very difficult for you.

Increase in earnings

It should come as no surprise to anyone that your Debt-to-Income will drop if you start earning more. Taking on overtime or changing to a better-paid job will definitely help, and using the increase to pay off your loans will be even more effective.

This way of reducing Debt-to-Income will not work if you are at your peak or your family situation does not allow you to spend more time at work.

Priority repayment of loans and credit cards

If your debts consist of a lot of small loans, for example for a phone, TV or computer, it is worth putting as much money as possible into paying them off quickly. Even if you incur an extra fee for terminating the loan early, you will free yourself from the problem, improving your financial situation once and for all.

**Always start overpaying on loans with the highest interest rates. **The second criterion is the time left to repay - if you have five instalments of £20 each left, it’s worth paying the whole thing back straight away.

Regular remortgage

If you already have a mortgage, remortgaging can help you lower your Debt-to-Income ratio. According to Get Rid of Rent, a reduction in interest rates of around 0.5 per cent means that the costs associated with getting a new, cheaper mortgage are usually recouped in less than a year. You can also use the lower mortgage rates to shorten the repayment period while keeping the same costs as before.

Unless something unforeseen happens, from June 2025 borrowers will start to feel the benefits of the series of interest rate cuts that the Bank of England is carrying out. It is at this point that it will be two years since the base rate exceeded 5.0%. It is currently 4.5% and you can believe us that half a percent makes a big difference when it comes to instalments.

Using financial surpluses to overpay loans

Not every time to overpay your loans is the same time. If you know you’re going to need to fix the engine in your car in three months’ time, which will cost you £800, it’s not worth focusing on paying off your loans quickly - it’s better to put some money aside so you don’t have to borrow to fix your car later. Even high Debt-to-Income is not a problem if you have savings for a few months ahead.

**If you don’t plan on spending anytime soon and you have some money for a black hour, allocating surplus funds to overpaying your mortgage, paying off credit cards or loans is the best investment you can make. **The rate of return is basically guaranteed and the risk is zero!

FAQ

Frequently asked questions

What is the debt-to-income ratio?

Debt to Income Ratio is the ratio of your monthly liabilities to your income.

What commitments affect the DTI?

Let us list the most important ones: Mortgages; Buy to let investment mortgages; Loans; Lease and hire purchase instalments (leases); Funds borrowed on credit cards.

Why is the Debt-to-Income ratio important?

The Debt to income ratio is an important factor from the perspective of the creditworthiness assessment made by bank underwriters.

Debt-to-Income and affordability?

According to most lenders, the maximum DTI is 60% and it is the factor that influences the amount you can borrow affordability, which is usually calculated as 4.

Debt-to-income and credit risk?

Your Debt to Income ratio does not directly affect your credit score.